Last week representatives from 50 community organisations from all over Australia travelled to Canberra to call on MPs to put a stop to the government’s “harsh” budget measures, including the move to tie pension increases to prices rather than wages.

According to the community groups’ joint statement, this change to pension indexation will “erode the value of the payments over time” and cause pensioners to “fall behind community living standards.”

The claim that indexing pensions to price increases will erode their value over time is wrong. The claim that it will cause pensions to fall behind community living standards depends upon whether one accepts that the current pension indexation system represents these standards, which is far from obvious.

At present, pensions—which include the Age Pension, the Disability Support Pension and Carer Payment—go up on the 20th of March and September each year, in line with the Consumer Price Index (CPI) or the Pensioner and Beneficiary Cost of Living Index (PBCLI) depending upon which has increased by the greater amount.

If, after indexation, the single rate of the pension falls below 27.7 per cent of Male Total Average Weekly Earnings (MTAWE), it is topped up to that amount, or 41.8 per cent for couples.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

The government’s proposal to remove the MTAWE benchmark—but keep CPI indexation in place—is estimated to save $331 million in 2017-18 and to reduce spending on the age pension by as much as $6.9 billion in 2024-25. It is an important aspect of budget repair.

Under the current system, in years when wages grow faster than prices, pensioners receive the benefit of this. In years when prices jump ahead of wages, pensioners are shielded from any reduction in the real value of their payment.

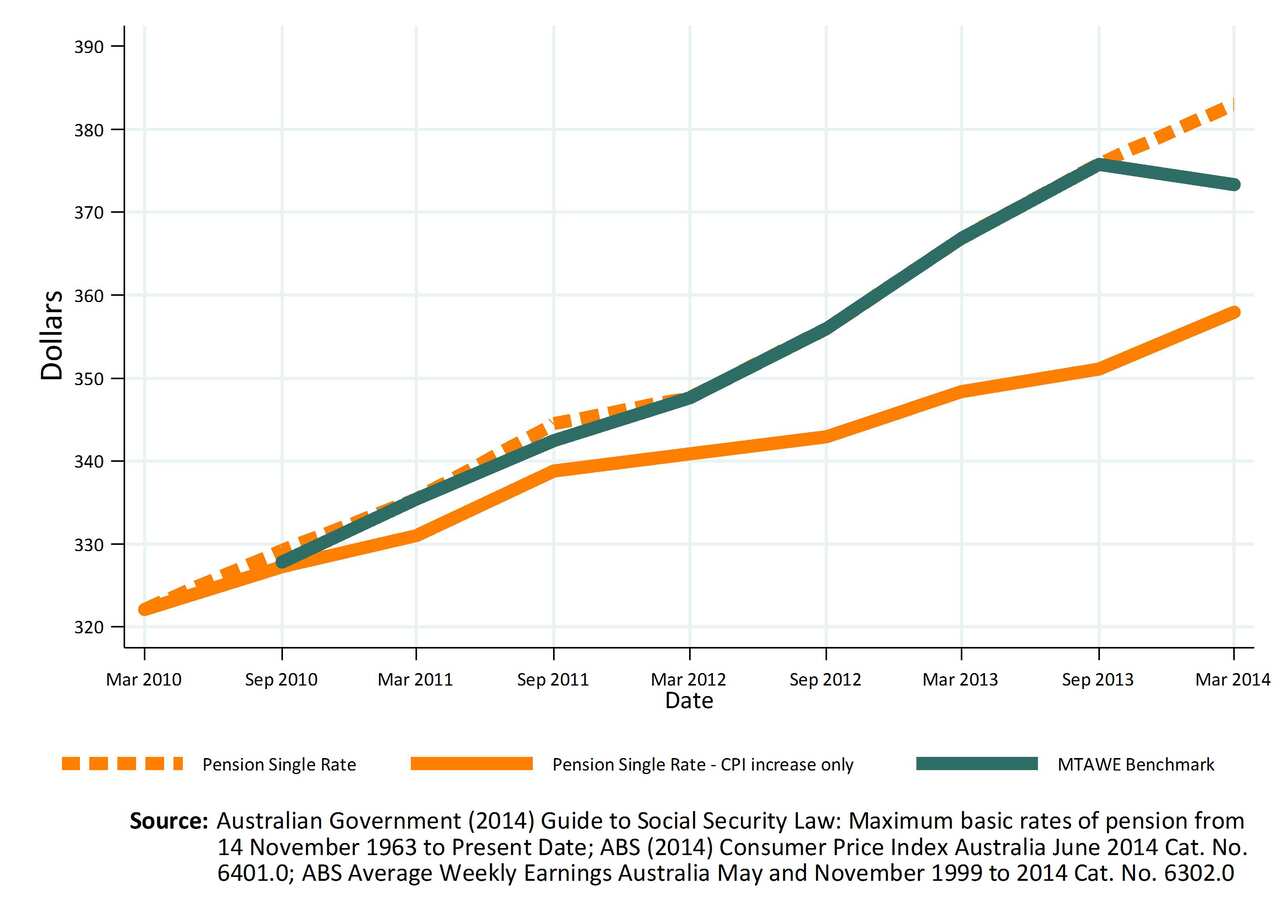

This can be seen in the following figure, which shows the increase in the weekly single rate of the pension from its March 2010 level of $322.10 per week. Also shown is a hypothetical estimate of how the weekly single rate would have increased had it only been subject to indexation by the CPI.

The amounts in the figure do not take into account the value of the Pensioner Concession Card, the addition of the Pension Supplement or the range of other goods and services provided to pensioners through other government programs.

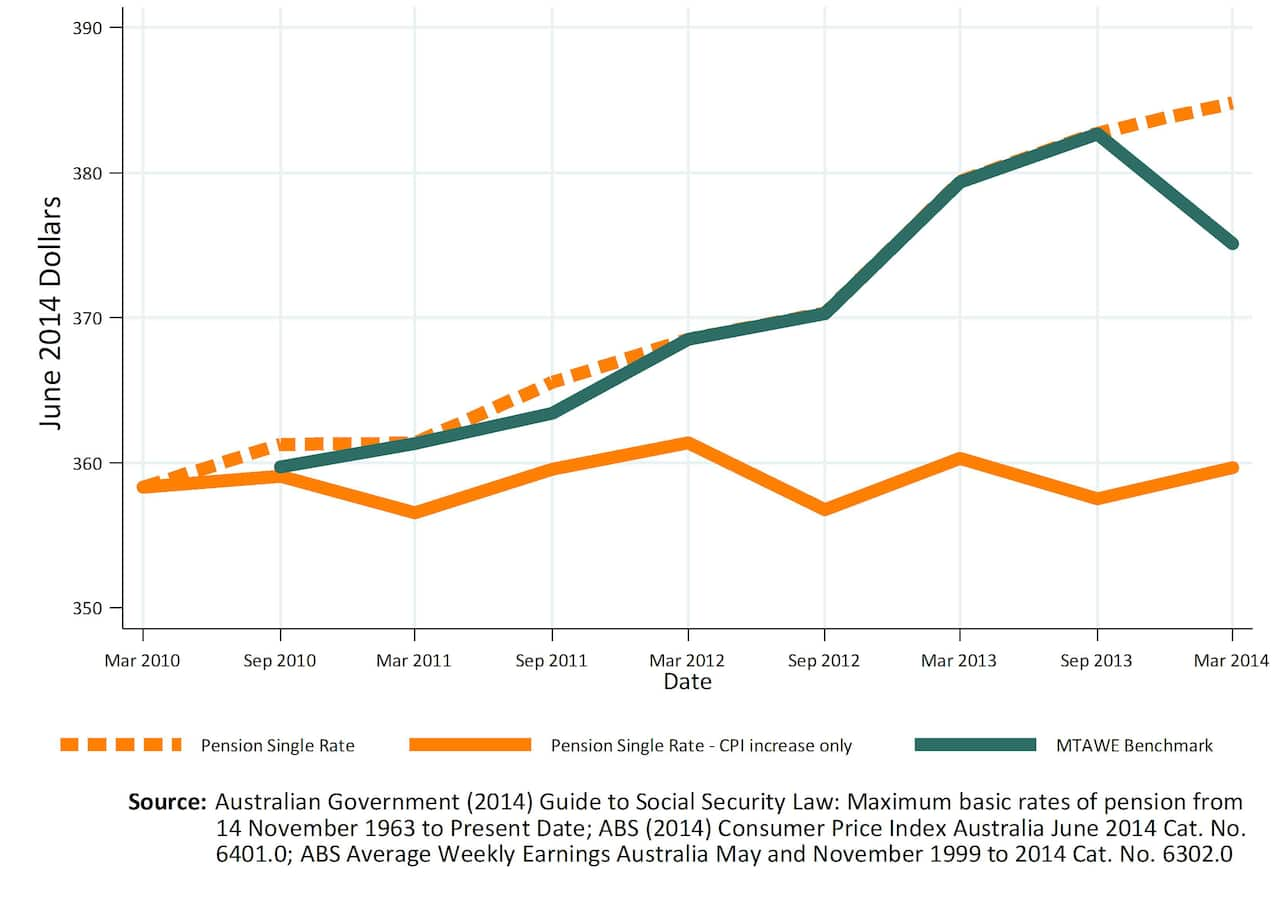

The next figure presents the same values in the previous figure but in March 2014 dollars. As is clearly shown, CPI indexation would have maintained the pension at $359 a week, on average—contrary to the assertion that CPI indexation would “erode the value of the payment over time.”

Proponents of the MTAWE benchmark argue that it is necessary so that pensions do not “fall behind community living standards,” but MTAWE is not a measure of any particular standard of living, let alone one that reflects a generally accepted community standard.

Even if one accepts that pensions should be tied to the living standards of wages earners MTAWE does not account for the taxes paid by wage earners and disregards the fact that 45.9 per cent of all employed Australians are women.

The 2009 Harmer Review into pensions and, more recently, the National Commission of Audit have described the MTAWE benchmark as an anachronism. This is being kind. MTAWE benchmarking has only been in place since January 1997, and even then women made up 43 per cent of employed Australians. Prior to that pensions were indexed to the CPI.

If the purpose of benchmarking is to reflect “community living standards,” then surely Australia’s 5.3 million working women are part of that community.

Rather than tying pensions to a multiple of gross wages, or to the average basket of goods that pensioners might have bought in the very distant past, a genuine community standard should be developed. This should be reviewed periodically to reflect changes in the pattern of consumption of pensioners with PBCLI indexation in between to account for increases in the prices of goods that they actually purchase.

It is easy to refer to community living standards when criticising budget measures. Far more difficult is defining what those standards are.

Matthew Taylor is a Research Fellow at the Centre for Independent Studies. He tweets @mattnomics.