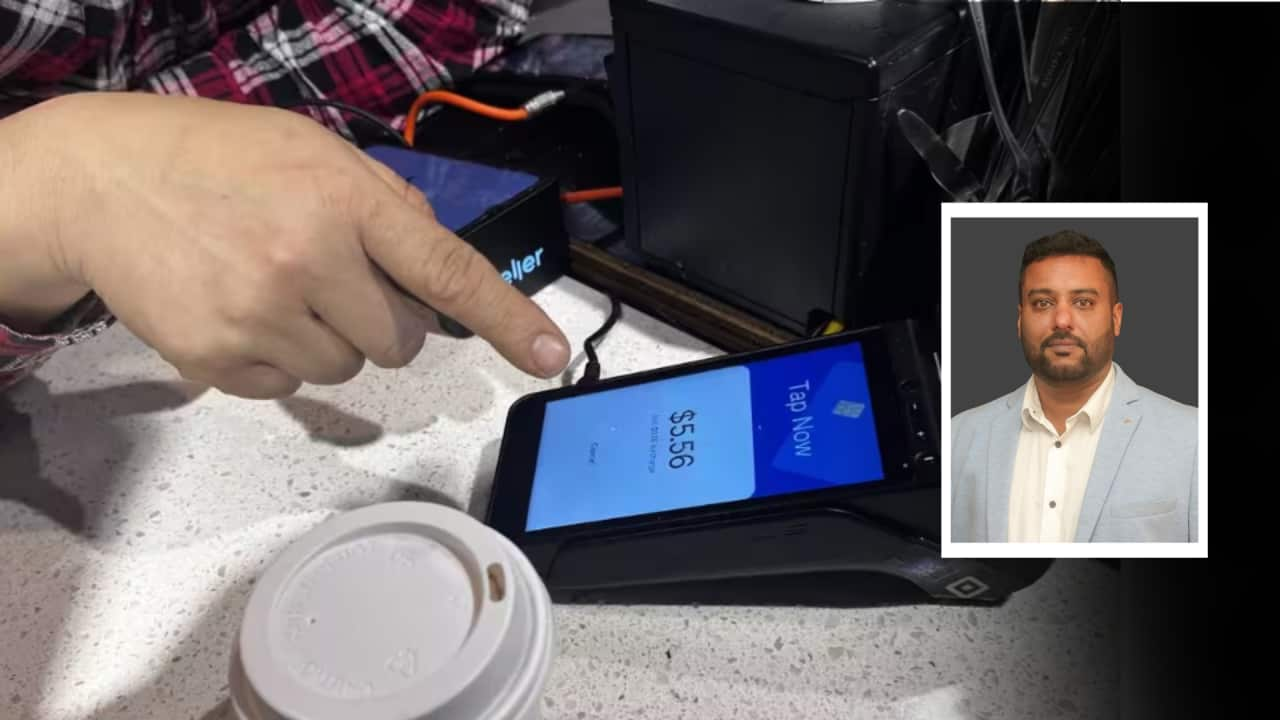

The extra cents added when you pay for a coffee with your card will soon be a thing of the past, as RBA announces reforms to remove surcharges on debit, credit and prepaid card payments across networks like eftpos, Visa and Mastercard from October 2026. In this podcast, we explore what this means for consumers, small businesses and the wider payments ecosystem, with insights from chartered accountant and fintech professional Sahil Kansal on potential savings, business impact and changing spending habits.

(The views expressed in this podcast are of the individuals. SBS neither agrees nor disagrees with them.)

Find our podcasts here at SBS Hindi Podcast Collection. You can also tune in to SBS Hindi at 5pm on SBS South Asian on digital radio, on channel 305 on your television, via the SBS Audio app or stream from our website.

Share