Australia's property price boom is being driven by record low interest rates and investors are taking advantage of cheap money in droves.

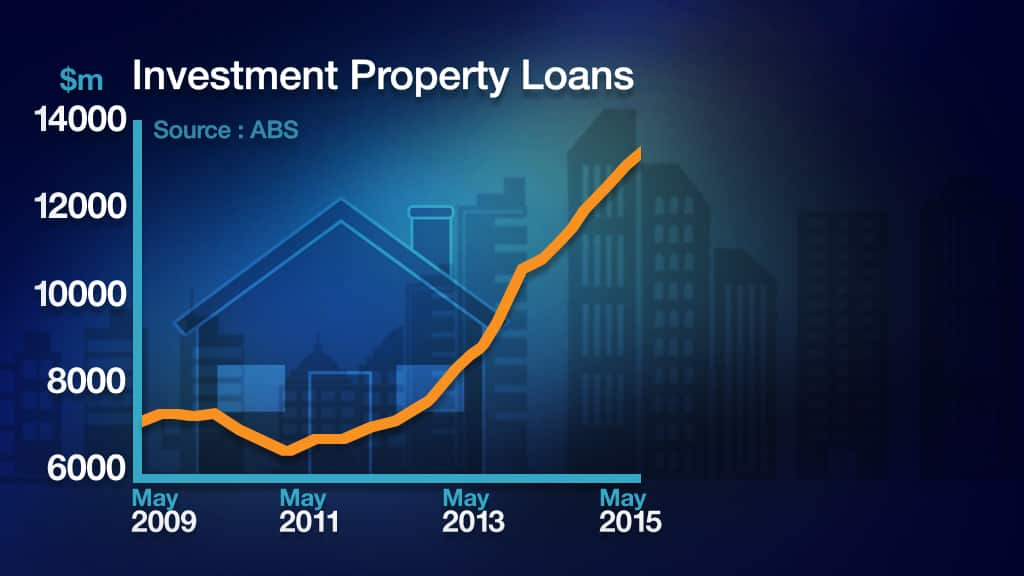

The Australian Bureau of Statistics says around $13 billion was lent to borrowers for investment property purchases in May.

The Reserve Bank is worried that sort of lending may be overstimulating the housing market and has worked with the banking regulator to limit what the banks can lend to investors.

As a result the country's largest financial institutions have been asked to keep total investor lending to 10 per cent.

One way they're doing that is by lifting variable interest rates on investment property loans.

ANZ was first on Thursday followed by the Commonwealth Bank on Friday.

The increase is basically the equivalent of a typical official interest rate move upwards by the Reserve Bank.

Macquarie Research said the move by ANZ will see earnings rise by as much as 1.6 per cent, but Westpac would stand to gain more, if it too followed suit.

For the banks and their shareholders, Macquarie Private Wealth Analyst James Rosenberg said it is good news.

"There'll be a small increase in earnings estimates for the big four banks, he said.

"Investment loans are only a small part of the overall loan book for these banks. I think we'll see small upgrades in the market and a slightly positive share price reaction but I would expect it to be significant."

For borrowers however, property buyer and agent Peter Wargnet says, it's a nasty shock.

"i think it will come as a surprise to existing investors in the market, partly because we need to remember there is a new generation of investors since 2010 which have only ever seen interest rates go one direction, this comes in conjunction with rental growth slowing to its slowest pace in nearly two decades so it's a double hit to some existing investors in the market."

Lifting investment property loan rates is just one way the banks can limit borrowing. Another is by making borrowers pay a larger deposit for their investment loan, which is also happening.

Peter Wargent says these strategies should help to meet APRA's requirements.

"That is the intention from the regulator. The market has become unbalanced between investor mortgages tracking at nearly half of all approvals, what APRA wants to see is the market becoming more balanced between owner occupier lending and investor lending," he said.

As for property investors James Rosenburg says it is a warning that rates can rise even when the Reserve Bank Board sits on its hands.

"I think investors taking up these types of loans need to be careful, they need to remember that interest rates are at record lows anyway and need to build in plenty of buffer into their calculations for any sort of loan," he said.

Interest rates on owner- occupier loans haven't been negatively impacted although some fixed rates have fallen slightly.