Australia's housing market is taking a long-expected breather after years of spectacular growth.

"People are saying, 'Is this the start of a major correction?', and the answer to that is no," says Alan Oster, NAB chief economist.

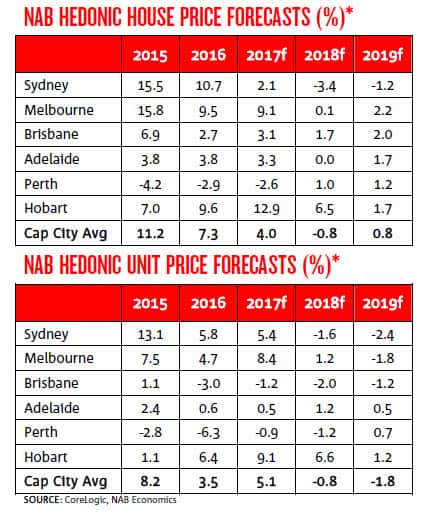

NAB has revised down its capital city house price forecasts for 2018 from a 0.7 per cent rise to a 0.8 per cent fall.

Of the capitals, Sydney's the only one predicted to see a decline in house values with Hobart forecast to outperform the rest.

Unit prices are set to fall in three capitals, including Sydney, Brisbane and Perth.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

Still, Oster says there's an undersupply in Sydney and Melbourne (although not as pronounced), interest rates are at record lows, owner-occupiers are generally years ahead on their repayments, and the employment market is healthy.

"If unemployment gets to about eight per cent, that causes grief, now across Australia, it's like 5.5 per cent," says Oster.

First home buyers have returned to the market, accounting for nearly 40 per cent of all new property buyers in the first quarter, a record high for the NAB Residential Property Survey.

Foreign buyers lifted from a six year low to 10.9 per cent.

But Oster says investors are playing less of a role.

"Owner occupier credit in the last 12 months is growing at eight per cent, and if you're looking at investor credit it's growing at 2.8 per cent."

Carlos Cacho, UBS Economist says it is that access to credit which some analysts say could impact future house price growth, especially if the banking royal commission recommends lenders apply stricter rules for borrowers.

"The main change we expect out of the royal commission is that the banks are going to have to do more due diligence when it comes to complying with responsible lending."

That's likely to mean a more detailed assessment of customer living expenses which may see borrowing limits fall dramatically.

"An average borrower can get about five to six times their income in a loan, we expect once tighter lending standards are introduced, and higher living expenses are used, that's probably going to fall to three to four times the income," says Carlos Cacho.

Less money to borrow means less offered for homes.

"It really depends on how tight credit gets, and how quickly that happens. But if we do see a credit tightening, then 10 per cent is not out of reasonable bounds."

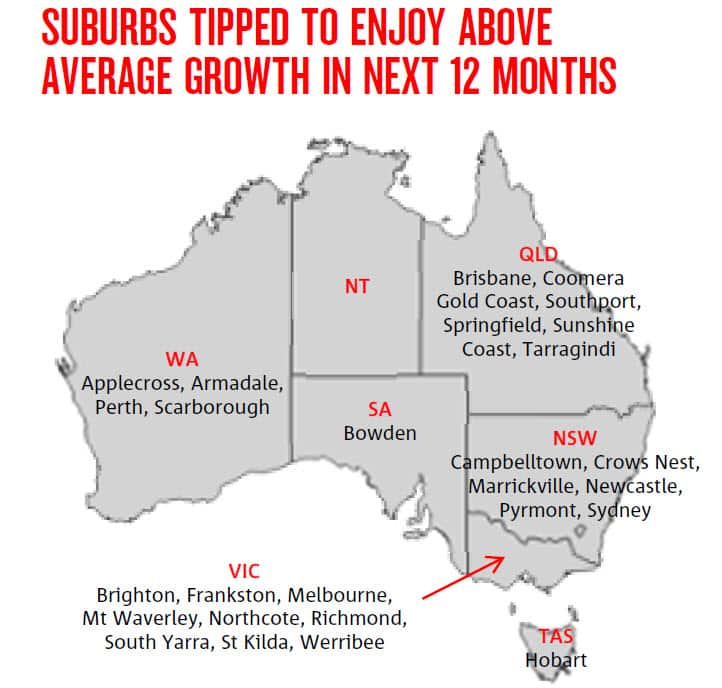

NAB does see some value in the market in strategic locations, across the country.

The royal commission will recommence public hearings on April 16.