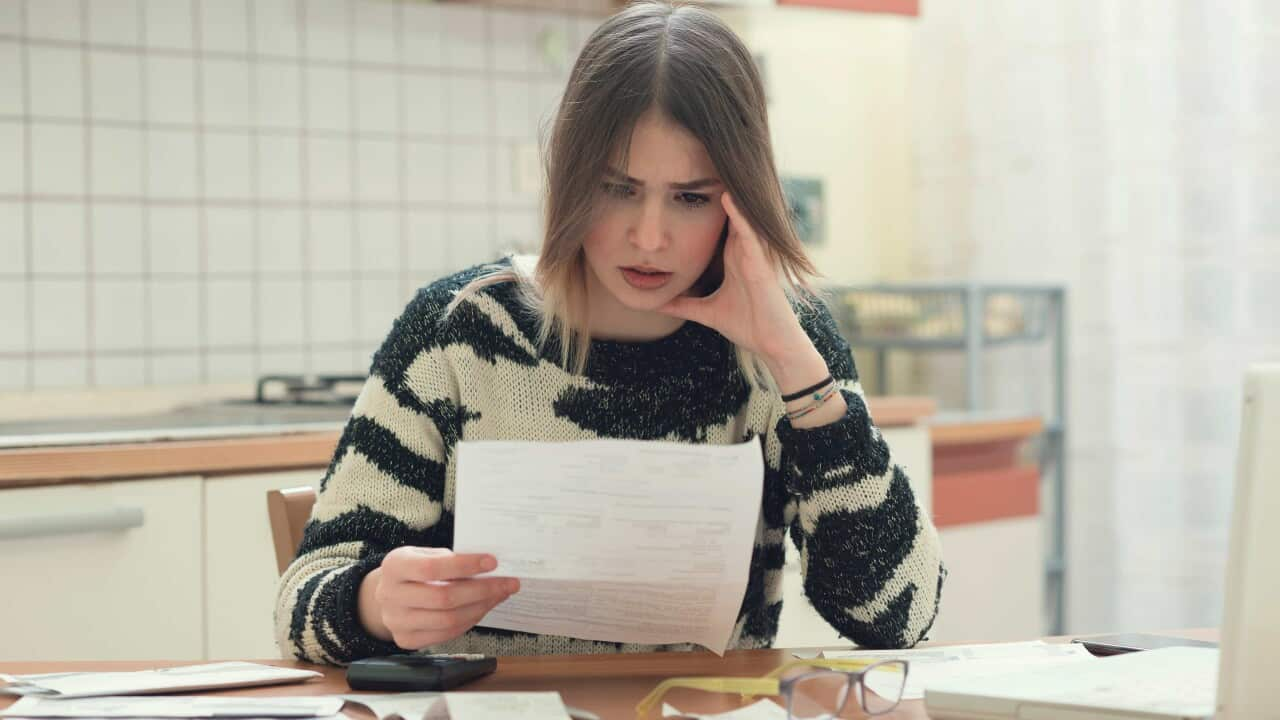

Australia’s first recession in 29 years has financial counsellors busy taking calls from people who have never faced debt problems, and there are concerns debt amid the pandemic may provoke serious mental health concerns.

Highlights

- The National Debt Helpline and Beyond Blue are finding that financial pressures are causing mental health issues.

- Most financial counsellors report that their clients are less stressed and more hopeful after seeking financial advice.

- Young people are more likely to resort to payday loans or personal loans to make ends meet.

The National Debt Helpline’s financial counsellor Sarah Brown-Shaw has spoken to thousands of people in financial crisis before, but the economic hardship caused by COVID-19 is unlike anything she she’d seen in previous years.

Many of the international students who would normally be working, prior to Australia’s first recession in nearly 30 years, are now asking for access to basic necessities such as food as they struggle to pay their tuition fee and rent.

Terrible. It doesn’t get much worse to be honest.

Recent consumer data released by the Consumer Policy Research Centres shows that seven in 10 young Australians are now concerned about their financial wellbeing.

Good Shepherd is one of Australia’s longest running charities providing microfinance products and services to the needy.

Its general manager of economic wellbeing and enterprises Megan McAlpine says her organisation is being approached by many temporary migrants who have been excluded from the government’s financial support schemes.

She says the people hardest hit by the ripple effects of COVID-19 are young people, new migrants and women.

Her observations echo recent consumer data showing that young Australians aged between 18 to 34 are three times more likely to have taken out a loan from a payday lender or consumer lease in July and are twice as likely to have taken out a personal loan just to make ends meet.

Many of the people work in industries that have been hardest hit like hospitality or the retail sector or people who are working part-time or have casual jobs.

Brown-Shaw says those with little or no income struggle to access loans – this is where financial counsellors like herself step in to come up with creative solutions.

One of the legal requirement when you borrow money is that the lender has to do an assessment to be certain that you can afford to make the repayment.

Brown-Shaw says this is when people who are in a desperate situation turn to quick and precarious lenders who do not carry out proper checks and assessments to the same standard as the banks.

She says those new to the country often are not aware of safer places to borrow where fees are not as high.

People are often going to payday loans or quick loans – there’s huge risk associated with those sorts of products.

The Financial Rights Legal Centre is part of the National Debt Helpline which provides free legal advice to those under financial stress.

While desperate times call for desperate measures, senior solicitor Jen Lewis warns people to avoid pay-day loans at all cost.

Lewis often gets contacted by distressed callers whose bank accounts run out of money for basic living cost after loan repayments are directly debited from their income or Centrelink payment.

Generally, those loans will have really high interest and fees. You are paying back often many times more than the original loan.

Some of the payday loans over $2,000 are often secured on an asset such as a car.

What that means is that the car itself is at risk of being taken if a borrower falls behind on their repayments.

The flow on effect is the inability to drive to work or drop the children to school as the car has been repossessed.

All of this means that you very quickly find yourself having to take out another payday loan to pay off the first one so that's when you’re really in a debt trap.

Brown-Shaw also cautions against other loan products such as the seemingly harmless after pay and the buy-now-pay-later schemes which provide easy access to multiple contracts.

With ten per cent of the Australian workforce expected to be unemployed by Christmas, many workers have either lost their job or had their hours reduced - significantly reducing a borrower’s ability to make regular repayments.

The minute you fall behind, that's when the lenders start hitting you with quite large fees and interests and charges.

McAlpine says another risky loan product to avoid is the rent-to-buy schemes which are promoted as a cost-effective way to access everyday essential items.

They are actually a really expensive way to purchase those goods with very high interest rates associated.

While consolidating all of your debt may sound attractive, Lewis urges people to seek financial counselling first from the National Debt Helpline.

Entering into a Part 9 Debt Agreement is actually of itself an act of bankruptcy. Generally, there are much better options for them.

Different to buy-now-pay-later schemes, payday loans are regulated by the National Consumer Credit Protection Act.

Jen Lewis says the Financial Rights Legal Centre can help consumers resolve their debt disputes if they believe they have been lent money that they couldn’t afford to repay in the first place or if the loan does not meet the borrower’s original requirements and objectives.

There is a free dispute resolution mechanism available to challenge that loan and if you are successful, you really only have to repay the principle.

Megan McAlpine says in addition to providing micro-financing options to those in financial hardship, Good Shepherd also provides no interest and no fee loans to non-permanent residents for things like white goods, washing machine, school needs, furniture and in some cases, medical bill.

That particular loan is for up to $1,500 and it’s for people who are on a health care card or for people who earn less than $45,000 a year and a lot of people access that loan.

Funded by the Australian government and the National Australia Bank (NAB), Good Shepherd also provides household relief loans for people who have lost their job due to COVID-19 to cover utility bills and rent for up to $3000.

Single borrowers will need to earn less than $60,000 or $100,000 if you have dependants to access the loan.

The loan is available to anyone who have a visa that expires after the term of the loan which lasts anywhere from 12 to 24 months.

Payments are made directly to the provider of the goods or the rental agency or the utility’s provider.

McAlpine believes a debt tsunami is already upon many in financial hardship due to a combination of a credit-based lifestyle prior to COVID-19 and the economic downturn caused by infection control measures.

McAlpine is critical of the credit industry which has made it easier for borrowers to access high risk loans such as Afterpay in recent years.

Then getting into further difficulties down the track where they are not able to then pay them back.

Brown-Shaw says making the first call to the National Debt Helpline is often the hardest step for people who have never experienced financial hardship.

Some are hesitant to call due to fear of their financial information being disclosed to their bank or employer.

But Brown-Shaw reassures callers that the helpline’s financial counselling service is free and confidential.

It’s completely non-judgemental, it’s completely confidential.

If you are under stress and need emotional support, contact Beyond Blue on 1300 22 4636

or Lifeline on 13 11 14.

For free and confidential financial and legal advice, contact the National Debt Helpline on 1800 007 007.

For more information or Good Shepherd’s no interest, no fee loans, visit its website or call 1300 121 130.

You can access your chosen service provider with the assistance of an interpreter by dialling the translating and interpreting service on 13 14 50.