“Rent money is dead money” or so the saying goes. It’s a popular myth perpetuated by plenty of people in the real estate industry. But when we did the sums, the reality was quite different.

The Reserve Bank of Australia (RBA) recently had similar findings to us: that since 1955, there hasn’t been much difference between renting or buying. Despite the constant news of property booms and million dollar sales in suburbs not known for being expensive, owners and renters over the last 60 years ended up in roughly the same place. That of course relied on renters being equally disciplined about saving, and investing those savings outside of cash deposits.

Like any financial decision, there are costs and benefits associated with buying and renting. We discuss some of the important pros and cons to consider when deciding whether to rent or buy, and work out which is likely to give the best results.

Buying

Pros of buying

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

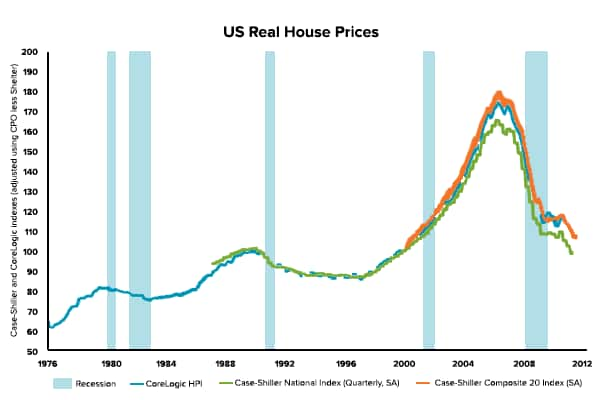

1) The appreciation (rise) in house prices over time. It’s hard to miss the stories that house prices have been rising, and fast over the past couple of years. The average Sydney property has risen 26% since the start of 2013 and other major cities haven’t been far behind. That’s great news for those that own. But while house prices have consistently risen over the long-term, they can also have periods of weak growth or even fall in value. During the financial crisis, house prices in the US fell by an average of 33.8%.

House owners also need to understand and be prepared to cope during periods of house price weakness.

2) Buying gives you the benefit of leverage. When you borrow money to buy a property, the bank lends a percentage of the purchase price to you. In Australia, banks often lend a high percentage of the total value which means the use of borrowed money to invest in the property, or the leverage, can be quite high.

For instance, it’s typical to contribute a 20% deposit and the bank mortgage covers the remaining 80%, or an 80% Loan to Value Ratio (LVR). Let’s say you buy a property for $500,000 with a deposit of $100,000 and borrow the remaining $400,000. If you sell the property a year later for $550,000, the property itself has risen 10% in value but your return on investment is 50% since you have made $50,000 profit on a $100,000 investment (i.e. the original deposit). That’s 5x leverage because you earned a 5x 10% return. It should be noted that after transaction costs, interest and principal repayments, the actual return is likely to be lower. Also, the opposite would be true if the house price fell from $500,000 to $450,000. Your profit would be -50% or worse after repayments and costs are accounted for.

3) Buying also provides some intangible benefits, like the security of not being displaced when the landlord decides to kick you out, and the flexibility to renovate the property.

Cons of buying

1) Interest repayments. If rent money is dead money then interest repayments are dead money too. Average variable interest rates are currently about 4.50% which means that you would pay about $18,000 a year on a $400,000 loan to buy a $500,000 house. That’s almost the same amount as the $19,500 you would pay to rent a similar value property for a year.

With interest rates at all time lows there’s a good chance that the rates in 5 or 10 years time will be much higher than now which means mortgage repayments could increase in the future. The RBA estimates that long term variable mortgage rates have been about 6.20% over the long term.

2) Opportunity cost. This is a cost that is often ignored or at least not understood very well. It refers to the cost of having your money tied up in a property versus having it available to use elsewhere. In simple terms, opportunity cost refers to the returns you could get elsewhere instead of putting down a house deposit. That could be returns from cash deposits (currently about 4%), a diversified portfolio (historically 8%), or investing in your own business.

3) Ownership costs. The transaction costs of buying and selling a property are high. The RBA estimates that the costs of buying a house including stamp duty and other buying costs including conveyancing can be 4.3% on average. The cost of selling a house including real estate agent commissions and advertising costs add up to about 3.0%. Therefore the total costs of buying and selling a house are in the vicinity of 7.3%. And this ignores the ongoing running costs of owning a property which the RBA estimates to be at least 2.6% per year including council rates, repairs, depreciation, body corporate fees, water and insurance costs.

Renting

Pros of renting

1) Return on your savings. Renting frees up your savings to earn a return elsewhere and depending on where those savings are invested, they may be able to earn a higher return than would be possible in property. This is the flip side of the opportunity cost of buying. Returns available in term deposits and savings accounts have been falling recently as the RBA has cut interest rates. This has made other investments like shares and bonds more attractive since bank deposit rates are now under 4% compared to a diversified portfolio of shares and bonds which has historically returned closer to 8% over the long-term.

2) Flexibility. While owning a property provides more stability, renting gives more flexibility. This may be attractive especially for young singles and families who may need to move from place to place due to work, due to bad neighbours or to try out different neighbourhoods.

3) Diversification. When you buy your own home, most (if not all) of your eggs are in one basket. One property in one suburb in one city in one country. That’s alot of your total wealth riding on a single investment that can be impacted by a whole list of factors outside your control. Renting allows you to spread that risk across a much broader range of investments.

Cons of renting

1) Rental costs. Renting costs have been steadily increasing in Australia. A typical rental yield (annual rent costs / house value) in Australia is now 3.9% but ranges from 2.5% to 5.0% depending on factors such as location, property value and whether it’s an apartment or house. Rent is the equivalent to interest you pay on a mortgage. It’s the cost of borrowing an asset – in the case of renting, the asset is a property whereas for a mortgage you’re borrowing money. Over the long-term, average rental yields have been 4.2% compared to an average variable mortgage rate of 6.2%. The current lower mortgage rates of around 4.5% have encouraged many to look at buying, however buyers should be factoring in higher average rates for a 30 year mortgage.

2) No forced savings. Unlike buying where you are forced to contribute to a mortgage each month (which includes interest and principal repayments), renting doesn’t encourage forced savings. This can make it tempting for renters to spend spare cash rather than setting it aside. However, technology has enabled services like Pocketbook and Stockspot to make it easy for consumers to budget, save and invest – so keeping up with homeowners is becoming easier for renters in Australia.

Buy vs Rent – the results

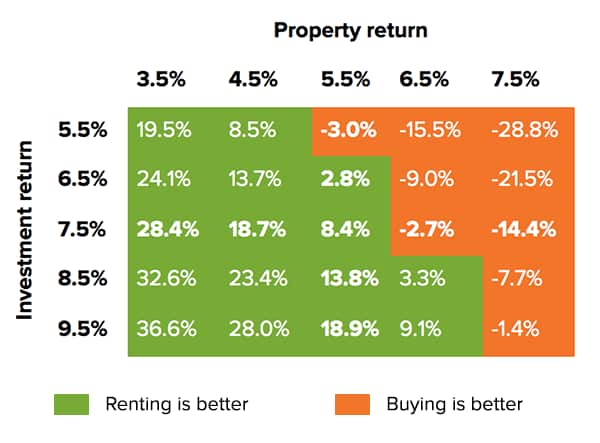

We have looked at whether someone would be better off buying, or renting and investing their savings in a diversified portfolio over the next 7 years. The results show the difference in overall financial position based on different possible return rates for property and investing.

A positive number shows where renting is better than buying and the percentage amount reflects the difference in returns over 7 years. Renting beats buying in 16 of the 25 scenarios and by 8.4% in our ‘base case’ of 5.5% property growth and 7.5% investment portfolio growth.

We have used a number of assumptions and different assumptions would impact these results. It should be noted that we have not considered the impact of ‘negative gearing’ which is a tax benefit that may be available if the property is held as an investment. Equally, franking credits on the share part of the portfolio have not been included in the investment returns. We also haven’t put a dollar value on the emotional benefits of owning or renting like security (owning) or flexibility (renting).

The case for buying

Over the last 3 years buying in major cities like Sydney and Melbourne has been a profitable strategy. Sydney prices have increased about 30% since January 2012 so combined with 5x leverage (80% LVR), investors in property would have enjoyed a return of nearly 150% on their initial investment.

What are the risks? Buying with leverage magnifies both the good and bad. So if you buy a Sydney property today with a 20% deposit (80% LVR), the property value would only need to fall 20% in value (i.e. where prices were less than 2 years ago) to completely wipe out the value of your initial investment. This happened to many property owners in the US between 2007-2010 when property prices fell by 33.8% between April 2006 and December 2011.

US homeowners that ended up with zero or negative equity after the property collapse and couldn’t keep up with interest repayments simply ‘handed back’ their house keys to their mortgage lender and their houses were sold to cover the loan. Where the funds recouped from sale were insufficient to cover the outstanding loan, the banks couldn’t go after the borrower for the subsequent loss because US loans are “non-recourse”. In Australia however, mortgage loans are “recourse loans” which means that the banks can chase you for any loss they incur when foreclosing your loan. This puts Australian borrowers at more personal risk in the situation of a property bust.

Australia was lucky to avoid a house price collapse during the financial crisis but that’s not to say it can’t happen here. Many academics and economists have been warning of the possibility of something similar in Australia. But provided it doesn’t happen and prices continue to increase, leverage will benefit those who own. Over the long term, the value of leverage is roughly equal to (annual return – mortgage interest rate) x leverage.

Example If a property returns 7%, interest repayments are 5% and leverage is 5x (500k property / 100k deposit) then your return is about 10%. That’s a solid return but relies on property continuing to rise more than mortgage interest rates. This will become more difficult as interest rates eventually rise from their 50-year lows.

The case for renting

Renting frees up your savings to invest elsewhere; either in term deposits, your business or a diversified investment portfolio. While rental yields are low (just 3.9% in Sydney compared to a long term average of 4.2%), it’s an attractive time to be renting and investing your savings somewhere else that could earn a higher return. This is why rent money isn’t really dead money – provided that savings are invested rather than spent.

Renting also enables you to avoid two big risks:

1) the risk of leverage which could mean your savings are overextended if property prices fall, and

2) the risk of poor diversification. When you buy, all of your eggs are in one basket so your wealth is almost completely reliant on the success of one asset. Renting allows you to spread those risks much more widely.

Our conclusion

Our analysis agrees with the RBA that renters are likely to be better off than property owners over the next 7 years based on long-term assumptions. This is consistent with the RBA’s assessment that Australian property is 19% overvalued compared to renting.

Prospective property buyers should think twice before jumping at the opportunity to sink their savings into a house. Leverage and poor diversification make home ownership much riskier than many people expect. The big benefit of a property mortgage has historically been the forced savings it encourages. But it’s now easier and more affordable to save without a mortgage. Renters today have more options than in the past to stay ahead.

Chris Brycki is the CEO and founder of Stockspot.