Sally Tindall, data insights director at the financial comparison site Canstar, told SBS News a rate cut is a good reminder to check in with your bank and ask if they will pass along the potential rate reduction.

"A cash rate cut is a fantastic time to look at your mortgage rate, ask your bank whether they're dropping that variable rate," she said.

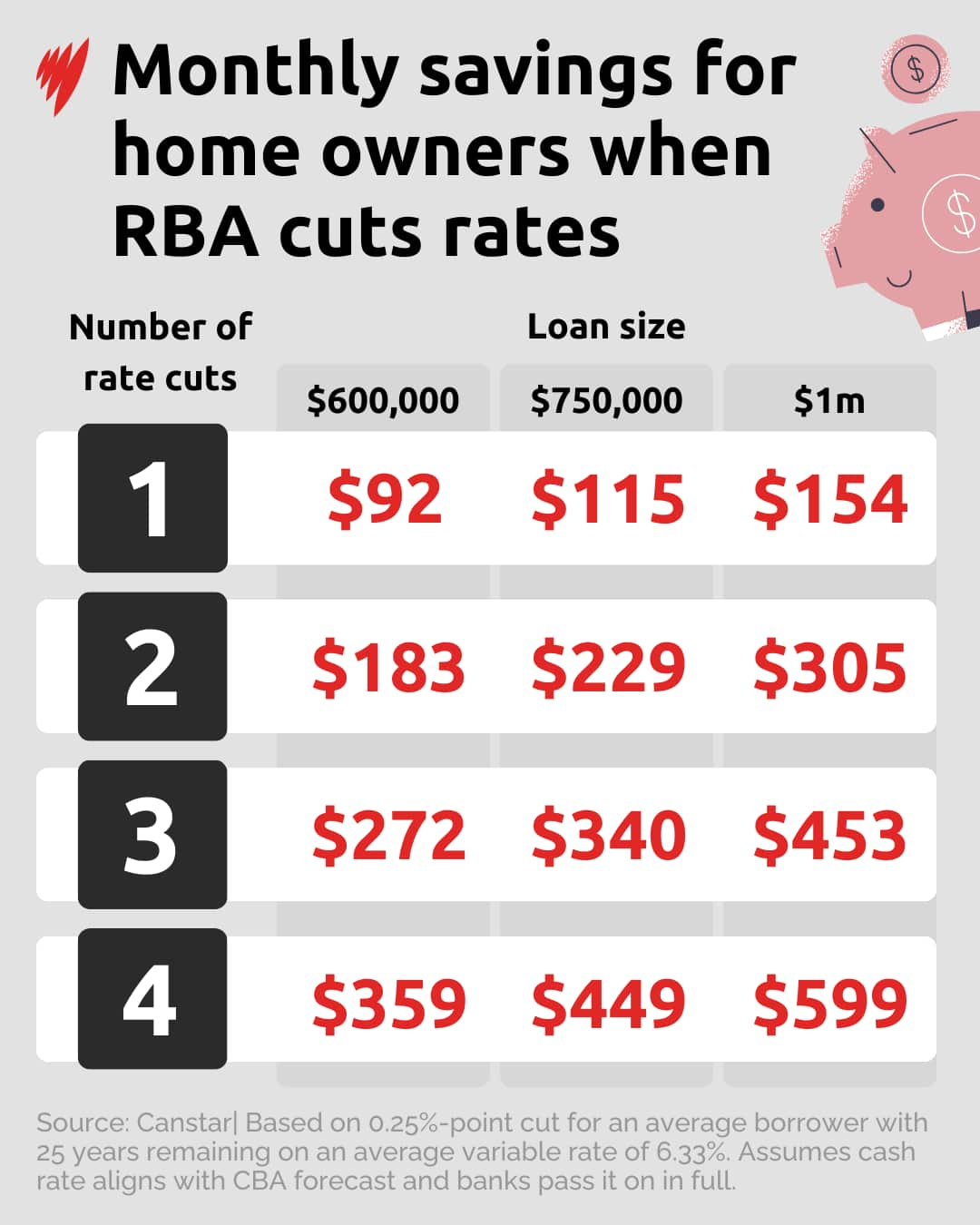

While there's no guarantee the banks will pass on potential cash rate savings, Tindall predicted a flow-on effect to mortgages.

Banks may allow mortgage holders to switch to lower repayments, saving them money in the short term, but this might not be in their best interest.

Graham Cooke, head of consumer research at comparison site Finder, explained paying more now can reduce the total amount you owe in the long run.

"My main piece of advice is — don’t automatically jump on the lower repayments option," he told SBS News.

"If you can afford it, keep the higher repayments. Each time you do that after the rate drops, it will shave about a year off your mortgage, over 30 years."

Renters are in a "trickier situation" at the negotiation table, but Cooke said landlords might be willing to reduce the rent in a competitive market.

"Interest rates going down is not an argument landlords or agents will typically accept for a rent reduction, unfortunately," he said.

"Instead, you're better off keeping an eye on rental listings around you and finding examples of similar properties that have lowered their rent.

"Present these to your landlord as evidence that you are paying too much and that they may struggle to find a replacement tenant willing to pay the same."

— Madeleine Wedesweiler and Cameron Carr

The information in this article is general in nature and is not intended as financial advice. You should consult with a licenced professional to make the decisions that are right for you.