Grace (surname withheld) was 18 when she took on a debt she didn't fully understand.

Drawn to a career in public policy, she enrolled in an Applied Public Health and Global Studies course. But the degree, which features science-heavy units — anatomy, physiology and laboratory work — cost far more than she anticipated.

"No one tells us about it," she tells The Feed of the HELP loan that funded it.

"When I was at school, I was naive … I didn't realise it was a loan that you have to pay back."

Now 24 and working as an executive coordinator at a public hospital, the recent graduate has watched her loan balance swing in ways that feel beyond her control.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

A one-off 20 per cent reduction to HELP (Higher Education Loan Program) debts and other student loans — a centrepiece of Labor's 2025 election pitch — stripped roughly $8,600 from her loan last year, taking it from about $43,000 to the low $30,000s.

But HELP debts are indexed to inflation annually on 1 June, and the most recent adjustment has already bumped her balance up again to around $35,000.

Grace has chosen not to make voluntary repayments, wary that any savings she contributes could simply be undone.

The average student loan in Australia sits at $27,640 and takes close to a decade — about 9.9 years — to clear in full.

With the onset of the new financial year, the benefit of a second, lesser-known reform is landing in the tax returns of Grace and roughly three million other Australians who still carry student debt.

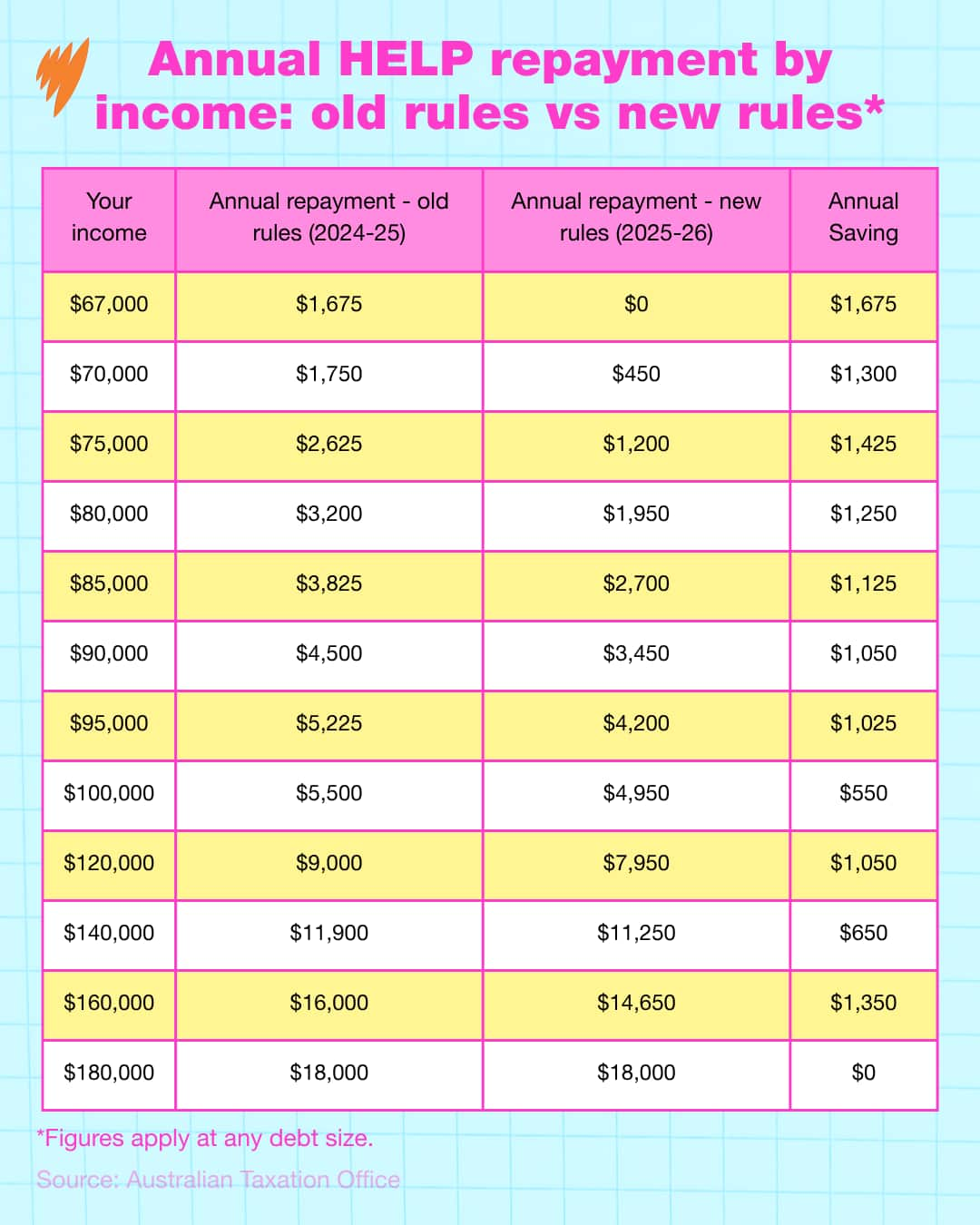

The repayment threshold — the income at which repayments begin — has risen sharply from $54,000 to $67,000, and repayments are now levied only on earnings above that threshold, rather than as a percentage of a person's total income.

The result: most borrowers will repay less each year, and those earning under $67,000 will owe nothing at all until their income rises.

Only those earning $179,286 and above continue to repay at the same rate as before — 10 per cent of their total income.

Accountant Scott Kay of Integrity Plus Accounting, who prepared the financial analysis behind this story for The Feed, describes the reform as "clever modelling by the government to help lower earners keep more of their cash in their pocket".

But what does the reform mean in real terms? And who comes out ahead?

A short-term win in every pay packet

For most borrowers — those earning between $67,000 and $179,286 — the headline change is less money withheld from their pay each fortnight.

Repayments apply only to the portion of income above $67,000, meaning those just above threshold benefit most. Previously, they paid a percentage of their entire income, rather than on the thin slice above the line.

The relief, however, does not scale evenly with income, and can even run in the opposite direction.

Under the old system, repayments were charged as a flat percentage of a person's total income, with that percentage jumping at fixed salary thresholds — so a small pay rise that pushed someone past a threshold could mean a higher rate.

The new system raises repayments more gradually, on a marginal basis, meaning the size of the saving depends on how heavily the old system would have taxed each earner.

Someone on $95,000, for instance, saves roughly $1,025 a year, while someone on $100,000 saves only $550 — not because they earn more, but because the old brackets treated their two incomes very differently.

Kay's modelling shows that lower earners still see the largest annual saving. A graduate on $75,000, for example, sees their yearly repayment more than halved to $1,200 — a saving of $1,425. Meanwhile, higher earners may only save a few hundred dollars each year.

For early-career workers with modest incomes, it means more money kept in each pay rather than quietly absorbed into a loan balance.

Accountant Sarah Clayton of Freshwater Taxation, a tax specialist who has examined the reform closely, agrees the short-term gain is both genuine and broadly felt.

The clearest beneficiaries, she says, "are likely to be graduates with smaller HELP debts, higher incomes, or strong future earning potential" — those whose debt was unlikely to linger long enough for a downside to take hold.

The catch beneath the relief

While loan holders will see more in their pay packets in the short term, for some, that relief comes at an extended cost.

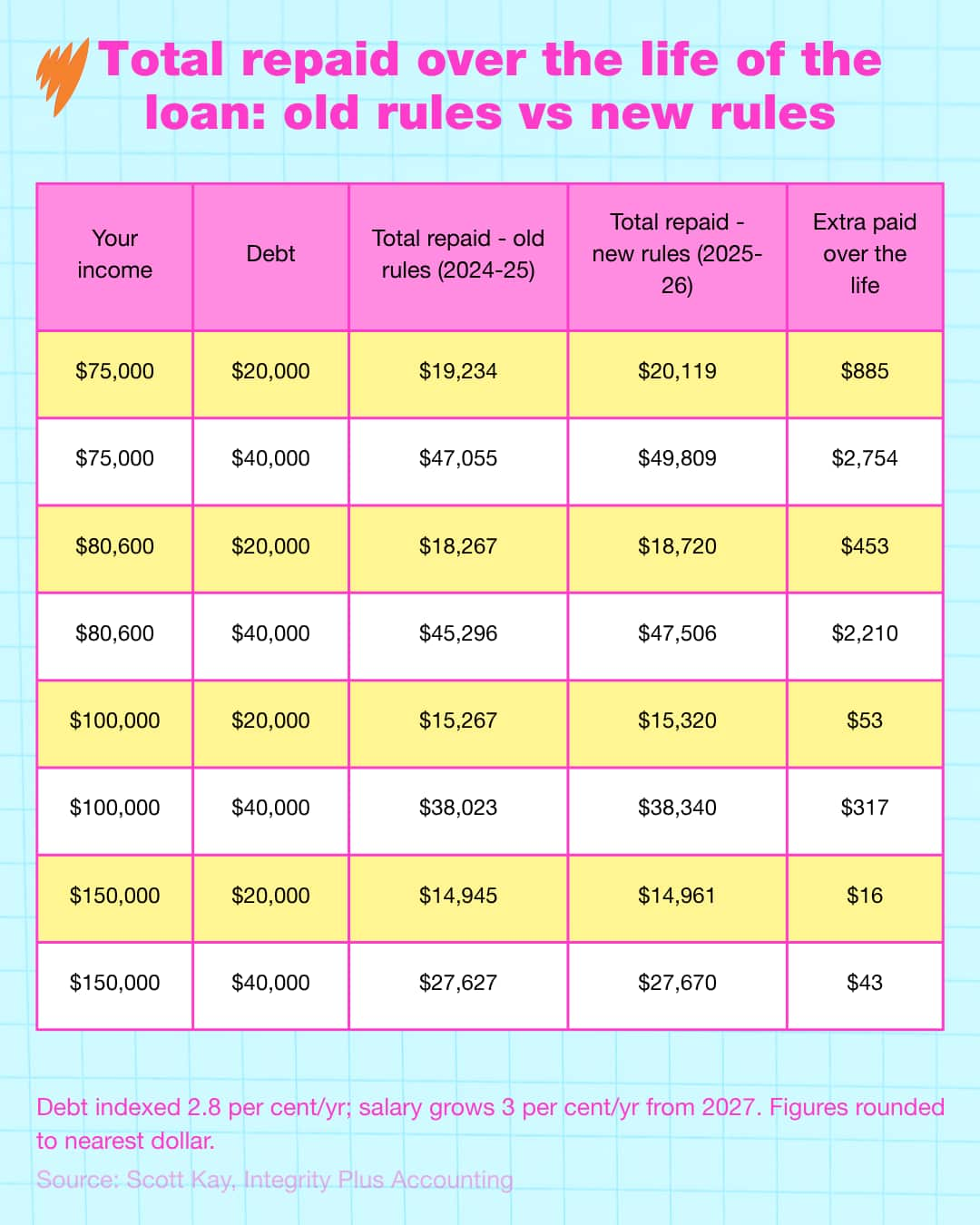

Because compulsory repayments are now initially smaller, the debt is paid down more slowly — and as HELP balances are indexed each year, a loan left outstanding for longer absorbs more indexation before it's finally cleared.

Modelling shows the burden is far from evenly distributed.

A graduate earning $75,000 with a $20,000 debt who would once have cleared it in six years now takes nine; raise that debt to $40,000 and the wait stretches from 12 years to 14.

A worker on $150,000, by contrast, clears even a sizeable debt in two or three years under either system.

Whether a borrower loses out, Clayton says, comes down to one factor: how long their income stays low.

The biggest losers are those whose incomes stagnate or fall — often because they have stepped back from full-time work to retrain, raise children or move into lower-paid sectors — leaving a large debt to sit and gather indexation for years.

But that profile is the exception, she says. Incomes generally rise over a career, and a graduate who starts on a modest salary and earns more with time will usually clear the debt before the additional indexation amounts to much.

The modelling prepared for The Feed assumes only a flat 3 per cent annual salary increase and so does not capture the larger jumps — promotions, pay rises and bonuses — that can clear a debt far faster than these figures suggest.

"If a person has an expensive degree, but then within a few years — a shortish amount of time — starts making good money, they're fine," Clayton says.

What ultimately decides the outcome is not the size of the debt today, but the trajectory of the income that follows it.

For Grace, who left Melbourne's suburbs for regional Queensland, the additional cash is welcome, but she feels somewhat trapped.

She now believes that staying there, where property is cheaper, is her only realistic path to home ownership. She is also in the process of retraining — a shift that will mean taking on more study, and with it more debt.

"I want to pay [my HELP debt] off as soon as I can," she says, "but am I going to pay off a $40,000 debt or am I going to pay my rent, eat every day, save towards a house?"

Who is actually better off?

The reassuring finding is that, across the full life of the loan, almost no one pays dramatically more — and the amount they do pay tracks income and debt with striking consistency.

A graduate on $75,000 carrying a $40,000 debt repays around $2,754 more over the life of the loan — the widest gap among the scenarios modelled for The Feed. A worker on $150,000 pays barely $40 more, whatever the size of their balance.

"Everyone is either the same or slightly better off," Kay says — no one repays meaningfully more, and many come out marginally ahead.

That cost is also tempered by a built-in safeguard. HELP debts now rise by whichever is lower, inflation or wage growth, so the balance can no longer climb faster than wages — as it did in 2023, when a spike in inflation pushed up debts sharply.

Kay points out that indexation has stayed relatively restrained — last year it sat at 2.8 per cent, with the highest rate in recent years in the 4s — so, for most people, a longer repayment period adds little to the total amount owed.

For most borrowers in the middle-income bracket, the exchange is simple: more money in hand now, for a loan that lasts modestly longer and costs modestly more.

However, there is also a pitfall Clayton flags for aspiring homeowners.

A HELP balance reduces how much a bank will lend, and a debt that endures for additional years shadows a mortgage application for just as long.

"The mortgage broker will always look at that debt. It will definitely go against them," Clayton says, noting some lenders insist the debt be cleared in full before they approve a loan at all.

For Grace, that concern is what weighs most heavily. "I do want to buy a house sometime in the near future," she says, "and I know that's going to be a very big factor in my borrowing capacity".

Yet her degree is not what she would undo.

"I don't regret it," she says.

"But I wish there was a different way young people can still have access to education."

For the latest from SBS News, download our app and subscribe to our newsletter.

Through award winning storytelling, The Feed continues to break new ground with its compelling mix of current affairs, comedy, profiles and investigations. See Different. Know Better. Laugh Harder. Read more about The Feed

Have a story or comment? Contact Us