This audio is voiced by AI and may occasionally mispronounce words.

Share your feedback and help us improve this feature. Read more about how we use AI at SBS here.

With the federal government ruling out higher taxes on gas exports, a long-running debate has resurfaced over who should benefit from Australia's vast natural resources — with Norway held up as the benchmark.

Critics of Australia's private sector-led resources sector argue Australians are not receiving a fair share from publicly owned minerals and gas, most recently pointing to claims that Australia's natural gas is being sold for "cents on the dollar".

The industry rejects this, arguing it is the country's largest corporate taxpayer and a key contributor to jobs, regional economies, and major infrastructure.

At the centre of the debate is a broader question about how resource wealth should be managed, with Norway often cited as an example of a resource-rich country that has structured its tax system so the benefits are shared more broadly.

Paul Cleary, an Australian journalist and author of Trillion Dollar Baby, a book on Norway's sovereign wealth fund, says the two countries adopted fundamentally different philosophies towards resource wealth.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

"When the Norwegians discovered oil … their approach was very much to say 'this is our resource, it belongs to us, and we're going to absolutely maximise all of the economic benefits out of it'," he tells SBS News.

"Whereas Australia's approach was to say, 'very free market, come and develop it, pay a little bit of royalties along the way, a little bit of tax, employ a few people, and we'll be happy'."

Tania Constable, CEO of the Minerals Council of Australia, says comparisons between Norway and Australia are like comparing "apples and oranges", arguing Australia already derives substantial public benefit through its existing tax and royalty system.

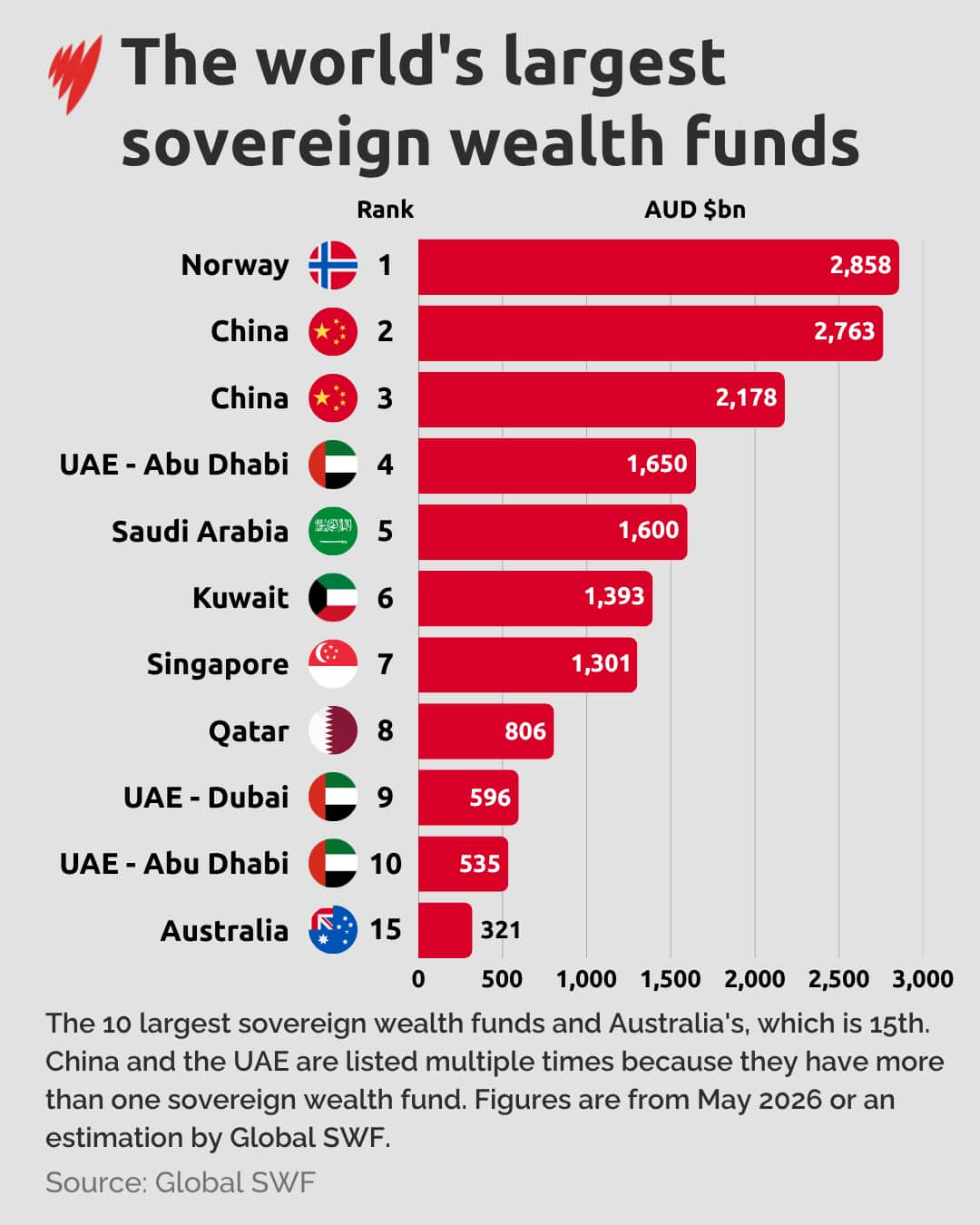

Norway, with a population of 5.6 million, levies a marginal petroleum tax rate of 78 per cent, with all the revenue flowing into a sovereign wealth fund now worth about $3.2 trillion — the largest of its kind in the world.

The Scandinavian country consistently ranks among the highest globally for living standards and funds extensive public services, including free tertiary education.

But the comparison with Australia remains contested, with economists noting that Norway's model was built under very different historical and institutional conditions, including early state participation in the sector and decades of policy continuity.

So how did Norway achieve this outcome, and are there lessons for Australia?

How Norway built its oil and gas industry

Before the discovery of oil and gas in its territory, Norway looked markedly different to the wealthy nation it is today, with an economy built on fishing, forestry, hydroelectricity, and shipping.

That changed in 1969, when the United States firm ConocoPhillips, then known as Phillips Petroleum, discovered the Ekofisk oil field in the North Sea, about 320km south-west of Norway.

It was a stroke of luck for the company. After more than two years of fruitless drilling and millions of dollars in losses, it was on its final test well.

The Ekofisk field would go on to become one of the world's largest offshore oil fields, followed by more than 100 other discoveries that transformed Norway into a fossil-fuel powerhouse.

But Norway's wealth was not simply the result of luck — it is also a product of how the country chose to manage its resources.

Many resource-rich nations fall victim to the "resource curse", becoming overly dependent on commodity exports and vulnerable to price shocks. Venezuela, which has relied heavily on oil exports, is often cited as a textbook example.

Others suffer "Dutch disease", in which booming resource exports drive up a country’s currency and weaken industries such as manufacturing and agriculture.

Norway largely avoided both, with economists attributing it to a combination of high taxation of oil profits and the decision to invest revenues offshore through a sovereign wealth fund rather than spend them directly in the domestic economy.

Strong democratic institutions and strict fiscal rules also helped limit corruption risks that have affected some other resource-rich countries.

The Norwegian parliament also adopted a set of principles known as the "10 Oil Commandments", which stated its petroleum resources should benefit Norwegian society as a whole.

Unlike Australia's more private-sector-led resources model, Norway's government deliberately had a strong role in petroleum development to retain public control over oil wealth.

In 1972, the government established Equinor — then known as Statoil — and introduced a policy requiring significant state participation in petroleum licences held by private companies.

Norway initially combined corporate taxes with royalties — payments made for the right to extract and sell oil — before introducing a dedicated petroleum tax in 1975.

Today, oil and gas companies face a combined marginal tax rate of 78 per cent, effectively comprising a 56 per cent petroleum tax and the standard 22 per cent corporate tax.

Crucially, the petroleum tax is structured as an investment-neutral tax on cash flow, not profit.

Costs are immediately deductible in the year they are incurred, and in some years, when the company records a loss, it is reimbursed by the Norwegian government. That encourages exploration and investment, as Norway shares some of the financial risk.

But when a company becomes profitable, Norway takes a larger proportion of revenue than it would from royalties.

How Norway turned oil wealth into a sovereign wealth fund

While high taxation and a state-led sector enabled Norway to accumulate vast wealth, policymakers were conscious that its natural resources were finite and that spending the revenue domestically could fuel inflation.

In response, it passed legislation in 1990 establishing a sovereign wealth fund, now known as the Government Pension Fund Global, with the first deposit made in 1996.

The fund was designed to serve three purposes: provide revenue for the national budget, preserve wealth for future generations and act as a rainy-day fund during economic downturns.

All net cash flows from the petroleum sector — including taxes, state ownership stakes and dividends from Equinor — flow into the fund, which invests entirely overseas to avoid overheating the domestic economy.

It is now worth a staggering $3.1 trillion — more than $500,000 for every man, woman, and child in the country — and boasted a return of $350 billion in 2025.

Norway now owns about 1.5 per cent of all listed shares worldwide, and more than half of the fund's value comes from investment returns rather than oil and gas tax revenue.

Norway did not make its first withdrawal from the fund until 2016. Under its fiscal rules, the government can spend only up to 3 per cent of the fund's value each year, although its sheer size now means it accounts for about a quarter of the national budget.

Australia also has a sovereign wealth fund, the Future Fund, currently valued at $337 billion.

It was established in 2006 to strengthen the federal government's long-term financial position by covering future unfunded public sector superannuation liabilities. Initial contributions were made from budget surpluses and proceeds from the partial sale of Telstra.

There are several smaller funds separate from the Future Fund but managed by the same board for medical research, disaster readiness and prevention, drought reduction, NDIS expenditure, and social and affordable housing.

How does Australia tax its natural resources?

Australia developed a far more market-driven resources sector, with governments preferring to tax and regulate extraction rather than directly participate in it.

Onshore minerals such as iron ore, coal, and gold belong to state and territory governments, but the private sector leads development and production. Companies pay royalties for the right to extract and sell resources, in addition to a flat corporate tax of 30 per cent.

Royalties differ between states and territories, as well as the type of minerals and by value or volume.

Western Australia, for example, charges a royalty on iron ore of between 5 per cent and 7.5 per cent of the value at the point of sale, depending on the level of processing and product type.

Offshore oil and gas resources are owned by the Commonwealth and are primarily taxed under the controversial Petroleum Resource Rent Tax (PRRT), a profit-only tax of 40 per cent.

Australia is not a major oil producer but is one of the world's largest exporters of liquefied natural gas (LNG). More than 90 per cent of Australia's natural gas comes from the north-west shelf off the coast of WA.

The PRRT allows companies to deduct capital expenses, such as building platforms or drilling wells, and carry forward unused deductions. As a result, in some years, gas companies pay little or no PRRT.

For example, US multinational Chevron's Gorgon LNG project cost about $70 billion to build and began production in 2016, but it did not make its first PRRT payment until 2025.

Critics of the PRRT say it is ineffective and argue Australia is losing out on billions of dollars in potential tax revenue each year. The PRRT raised about $1.4 billion in 2024-25, while LNG export revenues exceeded $65 billion.

In recent months, the Greens and independent senator David Pocock, among others, have been pushing the government to introduce a 25 per cent export tax on natural gas, based on volume, rather than profit. They have also called for some of the extra revenue to be directed into a sovereign wealth fund.

The issue came into focus during a Senate inquiry in February, when a Treasury official, under questioning from Pocock, confirmed Australia was collecting more revenue from the beer excise ($2.7 billion) than from the PRRT ($1.5 billion) this financial year.

A social media post by Pocock garnered nearly 10 million views, prompting critics to question why Australia was "giving away" its resources.

Energy companies, including Shell, Woodside and Chevron, say the sector paid $21.9 billion in taxes and royalties last financial year, and that it delivers economic benefits to Australia through investment, jobs and superannuation returns.

Despite the Senate inquiry finding weaknesses in the PRRT, Prime Minister Anthony Albanese has dismissed calls for a higher gas tax, saying it would jeopardise relationships with trading partners already facing energy shortages caused by the war in the Middle East.

A similar debate played out in 2010 during the mining boom, when then-prime minister Kevin Rudd proposed a "super profits" mining tax.

It was fiercely opposed by the Opposition and mining sector, with Rudd removed as prime minister in part by the campaign, despite polling suggesting many Australians believed mining companies were under-taxed.

A watered-down version of the super profits mining tax, known as the Minerals Resource Rent Tax, was later introduced by Rudd's successor, Julia Gillard, in 2012 before being repealed by the Coalition government under Tony Abbott in 2014.

Some economists argue Australia did not make the most of the mining boom, which peaked in the mid-2000s to early 2010s and generated an estimated $180 billion in additional revenue, according to analysis by the progressive think tank Per Capita.

While some of the windfall contributed to the Future Fund, the report found that much of it was instead used to reduce government debt, fund cash payments such as the baby bonus and first-home grants, and deliver tax cuts and concessions.

Independent economist Saul Eslake argues that budget surpluses during the mining boom — Australia recorded 10 between 1996–97 and 2007–08 — could instead have been directed into a dedicated sovereign wealth fund separate from the Future Fund.

Had those surpluses been invested, he says, Australia's fiscal position, which is now approaching $1 trillion in gross federal debt, would be stronger and better positioned to absorb economic downturns, such as the COVID-19 pandemic.

"At the time the government said, 'well, we're running budget surpluses, so fiscal policy is tight, and what more should we do?'" he tells SBS News.

"That opinion was accepted by a majority of economists and by a majority of the population. [Economists Chris Richardson, Ross Garnaut and I] saw it as an opportunity forgone, and having foregone it, we can't really get it back."

The political fork in the road

The divergence between Norway and Australia was not simply about tax policy, but rather fundamentally different ideas of ownership, the state's role, and who should benefit from natural resources.

So how did Norway and Australia arrive at such different positions?

Einar Lie, a professor of modern economic and political history at Oslo University, says Norway's approach is rooted in its political culture defined by high trust in government, low corruption and the belief that natural resources should benefit society as a whole.

"The core, I would say, of understanding the Norwegian approach … is that the resources to some extent belong to the state and should be taxed," he tells SBS News.

Unlike Australia, where resource taxation remains a live political issue, Lie says Norway's oil taxes are no longer a matter of public debate.

The same principle applies to other resources, such as fisheries. In 2023, Norway introduced a controversial resource rent tax on farmed salmon and trout, based on the argument that the highly profitable industry utilised the country's publicly owned coastal waters.

Fish farmers fiercely opposed the tax, but Lie says he does not expect future governments to reverse it.

"The independence of the state from business interests is quite vital," he says.

When Rudd proposed the super profits mining tax in 2010, the mining industry responded with a $22 million advertising campaign warning that the tax would cost jobs and drive investment offshore.

Lie says there was a similar response in Norway when the country introduced its petroleum tax in 1975.

"[The tax] was met with very strong criticism from the oil companies, both national, but especially the large multinational oil companies, that was American companies," he says.

But he says the Norwegian government held firm.

"They calculated in a cold manner that they would have a maximum tax rate, that they wouldn't set so high that the oil companies would leave the Norwegian continental shelf," Lie says.

"That was really the only boundary they had."

Ole Bjørn Røste, a professor of political science at the Norwegian University of Science and Technology, says another factor in Norway’s ability to impose a high petroleum tax was that major international oil companies had already made substantial investments in the North Sea.

"The big American companies were in there, there were sunk costs in business terms, and they saw a future in the North Sea, and therefore were willing to invest more, even if the tax was perhaps a bit unpalatable by American standards," he says.

Norway's left-wing Labour Party was in government for much of the 1970s when the petroleum industry was taking off, Røste says, meaning it was natural for the state to play a greater role in the sector.

Journalist Paul Cleary says the political fallout from Rudd's failed mining tax had a lasting impact on the debate around resource taxation in Australia.

"That episode showed the absolute power and influence of the mining industry in this country, that they were able to run a $22 million advertising campaign and effectively remove a first-term prime minister from office," he says.

However, Tania Constable from the Minerals Council of Australia says comparisons between Australia and Norway are unfair.

She says Norway's built its petroleum industry by having the state take on significant financial risk through its majority-owned oil company, Equinor (formerly Statoil), whereas Australia's natural resources sector took on huge risks, with only "one in 1,000 projects" getting off the ground.

Claims that the resources sector did not pay its fair share of tax are also not true, she says.

"It's the largest taxpayer by a country mile, compared to other industries," she says.

Rewards have to be there for companies that are investing in Australia, so profits are important, but every Australian benefits by a project getting on the ground.

According to the Australian Tax Office, Australia's mining, energy, and water sector paid $48.5 billion in company tax in the 2023-24 financial year — just over half of all corporate tax paid by large businesses.

A further $27 billion was paid in state and territory mineral royalties.

Can Australia do it differently next time?

While the government has ruled out any changes to gas taxation and is unlikely to adopt Norway's state-owned resources model, it is taking a more active role in critical minerals and the green energy transition.

Australia is rich in critical minerals such as lithium, rare earths, and nickel — essential for batteries, renewable energy infrastructure and electric vehicles — and global demand is expected to surge over the coming decades.

Last year, the government announced its $22.7 billion Future Made in Australia plan, aimed at building domestic renewable energy industries, including green hydrogen production, critical minerals processing, and clean energy manufacturing such as batteries and solar panels.

Australia also signed a $13 billion critical minerals deal with the US last year, designed to fast-track projects, strengthen supply chains and reduce reliance on China.

In a paper published last year, economists Russell Smyth and Joaquin Vespignani argued for taxation reform coupled with a sovereign resources fund directly linked to superannuation accounts and higher education funding.

"The clean energy transition — and resulting surge in demand for critical minerals — presents an unprecedented economic opportunity for Australia, given Australia has a high proportion of proven reserves," they wrote.

Constable says demand for traditional commodities such as iron ore and coal will continue, but the critical minerals sector offers an opportunity to build on Australia's existing resource base.

She says windfalls from higher commodity prices could be banked for the future through a sovereign wealth fund.

[The resources industry's] long-term legacy is wealth for the nation.

"Anything that is over and above those forecasts could go into a sovereign wealth fund and start to create something that can be utilised for the future."

For the latest from SBS News, download our app and subscribe to our newsletter.