In brief

- Patricia Nicula has just bought her first home in Queensland, along with her husband Tai, becoming the first members of their families to become homeowners.

- The value of an entry-priced home has risen steadily over the last five years along with inflation, while wage growth has lagged.

While the federal government's deposit scheme has helped some first home buyers get into the property market, the time it takes to save a deposit has still blown out for others as the cost of entry-level properties surges, a new report shows.

First home buyers are now facing a "dual affordability constraint", the report states, meaning deposits are taking longer to accumulate and repayments remain at near unaffordable levels for some once they've bought a property.

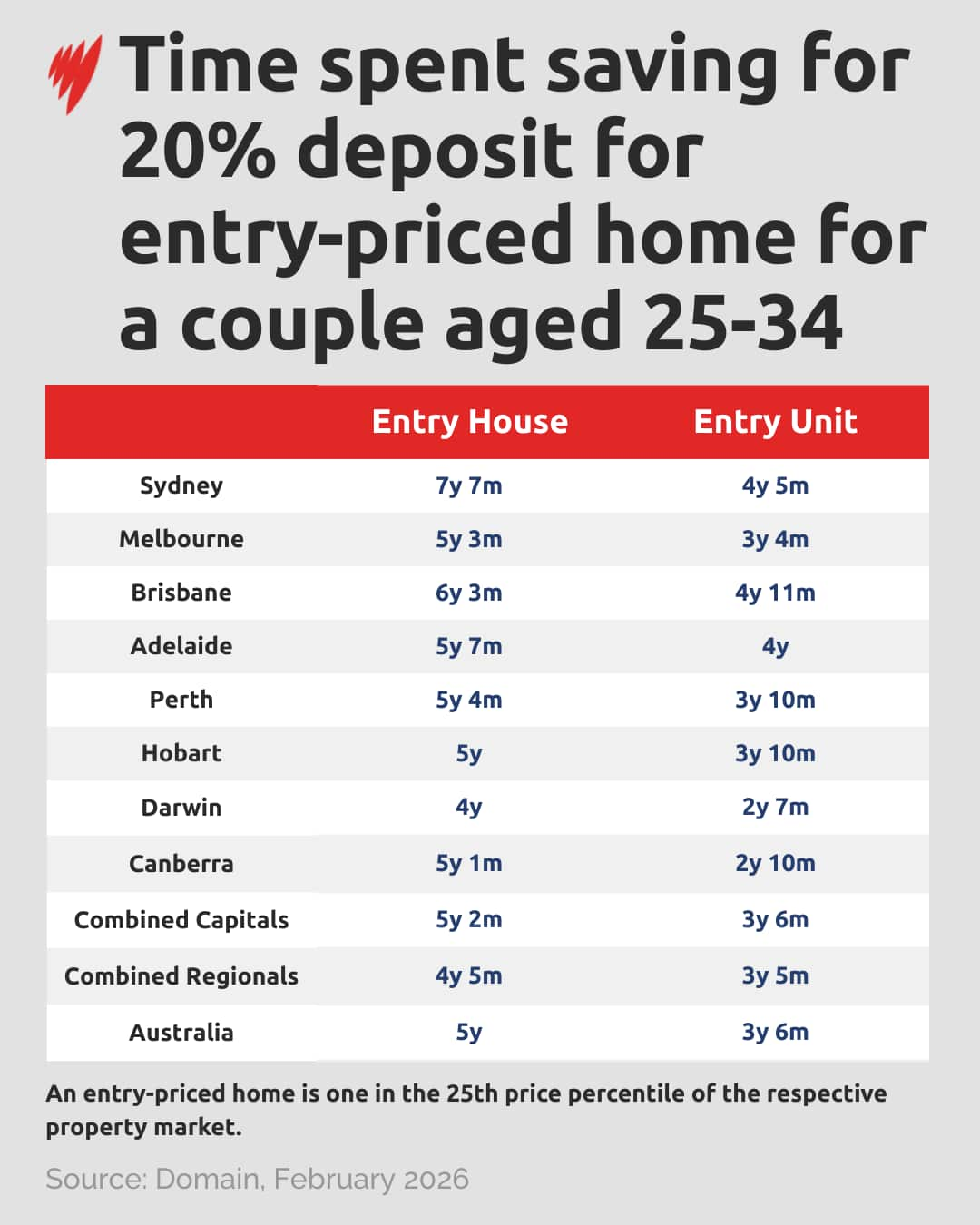

The time required for a couple to save a 20 per cent deposit now ranges from two years and seven months for an entry-priced unit in Darwin to seven years and seven months for an entry-priced house in Sydney, according to Domain's latest study released on Thursday morning.

These wait times can double for single-income households trying to climb their first rung on the property ladder.

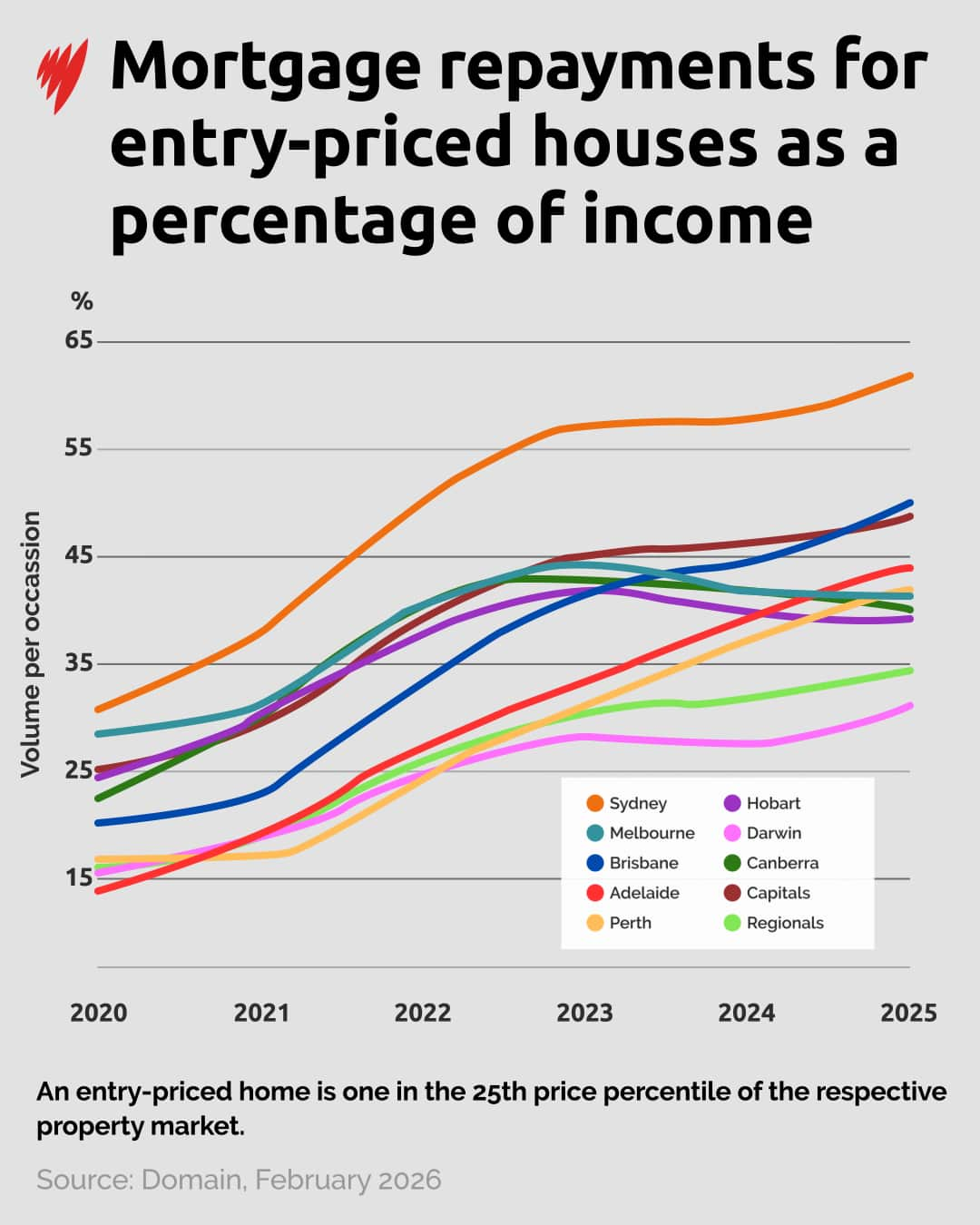

The report warns that even once a deposit is secured, first-home buyers are spending as much as 60 per cent of their income on mortgage repayments.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

Domain chief of research and economics Nicola Powell, told SBS News every capital city is now facing mortgage stress for people buying entry-level houses.

"We have seen multiple years of continuous price growth at that entry level price point, and that really has exceeded wage growth, not for one year, but for many years now," she said.

"It really does place pressure on first home buyers gaining access to Australia's housing market."

Data from the Australian Bureau of Statistics shows that since the government introduced new laws to allow buyers to purchase a home with just a 5 per cent deposit in October, more buyers are entering the market.

The number of new first home buyer loans rose 6.8 per cent to 31,783 in the December quarter 2025, according to the Australian Bureau of Statistics, up from 29,772 the previous quarter, and 29,132 the year prior.

Patricia Nicula has just bought her first home in Queensland, along with her husband Tai, becoming the first members of their families to become homeowners.

But it wasn't easy.

"It's definitely a very proud feeling and exciting at the same time. It's like we've got it all in the palm of our hands now, and it's just onwards and upwards from here," she told SBS News.

Property market 'overwhelming'

Nicula said that the process of looking for a home they could afford was overwhelming and stressful at times.

The pair saved for years to secure a deposit big enough for their first mortgage.

On average, a couple aged between 25 and 34 spends five years to save a 20 per cent deposit for their first house in Australia. In parts of the country, time spent waiting is closer to seven years.

"Although saving times have risen for both property types, the gap between houses and units remains substantial," the report reads.

The 29-year-old said the pair couldn't have afforded the property without the newly expanded five per cent deposit scheme.

"In today's economy, it's hard to save up for a huge deposit and let alone for seven years, so much can happen in seven years. That money might have to go somewhere else," she said.

After consulting with Queensland-based brokerage, Low Deposit Homes, Nicula said she better understood her borrowing power and decided to opt for the five per cent deposit scheme.

The pair settled on their first home in December.

"It's definitely a pinch me moment," Nicula said.

Is the new scheme making a difference?

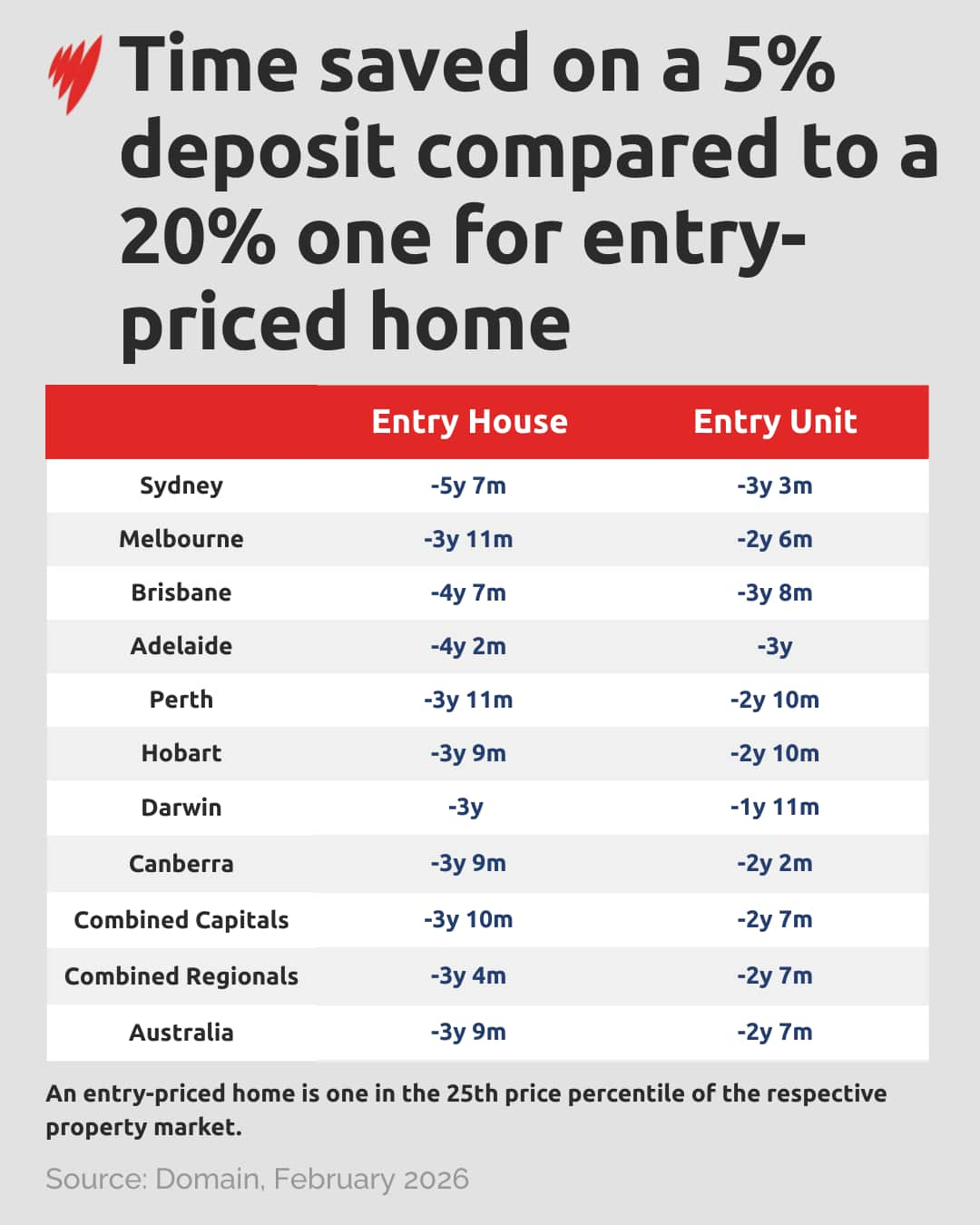

Domain estimates that accessing the five per cent deposit scheme has reduced the time it takes to save for a house by just under four years.

AMP chief economist Shane Oliver told SBS News the five per cent deposit scheme has been popular for first-home savers but could also come with downsides.

"You're going to find a lot of buyers trying to get in through this avenue, bringing forward demand and it could lead to competition in the property market, which has the effect of pushing prices up."

He said the increase in property prices saddles first-home buyers with larger mortgages and ultimately debt.

"You can get a five per cent deposit in just a few years. But you will have 95 per cent of your debt to pay off, that's a very high level of debt."

However, for some people, it may be better financially to buy a property sooner, as the market could move against you while you save a 20 per cent deposit, he added.

Chaise Paterson, a director at Low Deposit Homes, told SBS News the five per cent deposit scheme has led to "incredible changes".

"It's definitely opened up the opportunities for people to be able to buy, and one of the benefits that they have had with the changes that they implemented was the much higher property price caps and then also to removing the income caps," he said.

Previous income caps weren't adequate with higher property prices, he explained.

He said the added flexibility was beneficial overall in helping people purchase their first property and to start building equity.

"If you are sitting there for 10 years to save up a 20 per cent deposit, you're continuously paying rent during that period of time," he said.

How much are people spending?

The value of an entry-priced home has risen steadily over the last five years along with inflation, while wage growth has lagged, leading Australians to spend more of their income on mortgages, Domain's research showed.

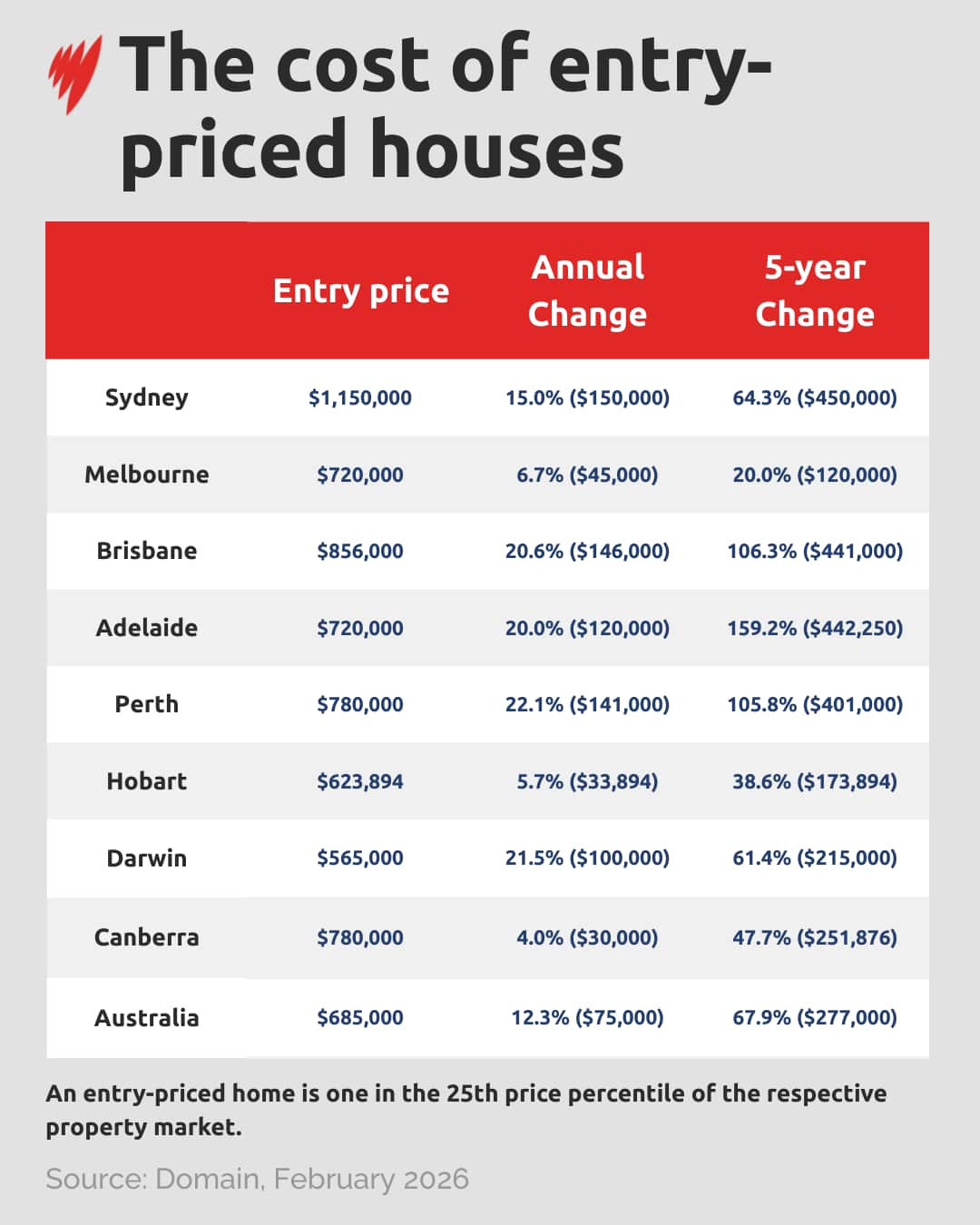

The cost of an entry-priced house has increased by 68 per cent nationally over the last five years to $685,000.

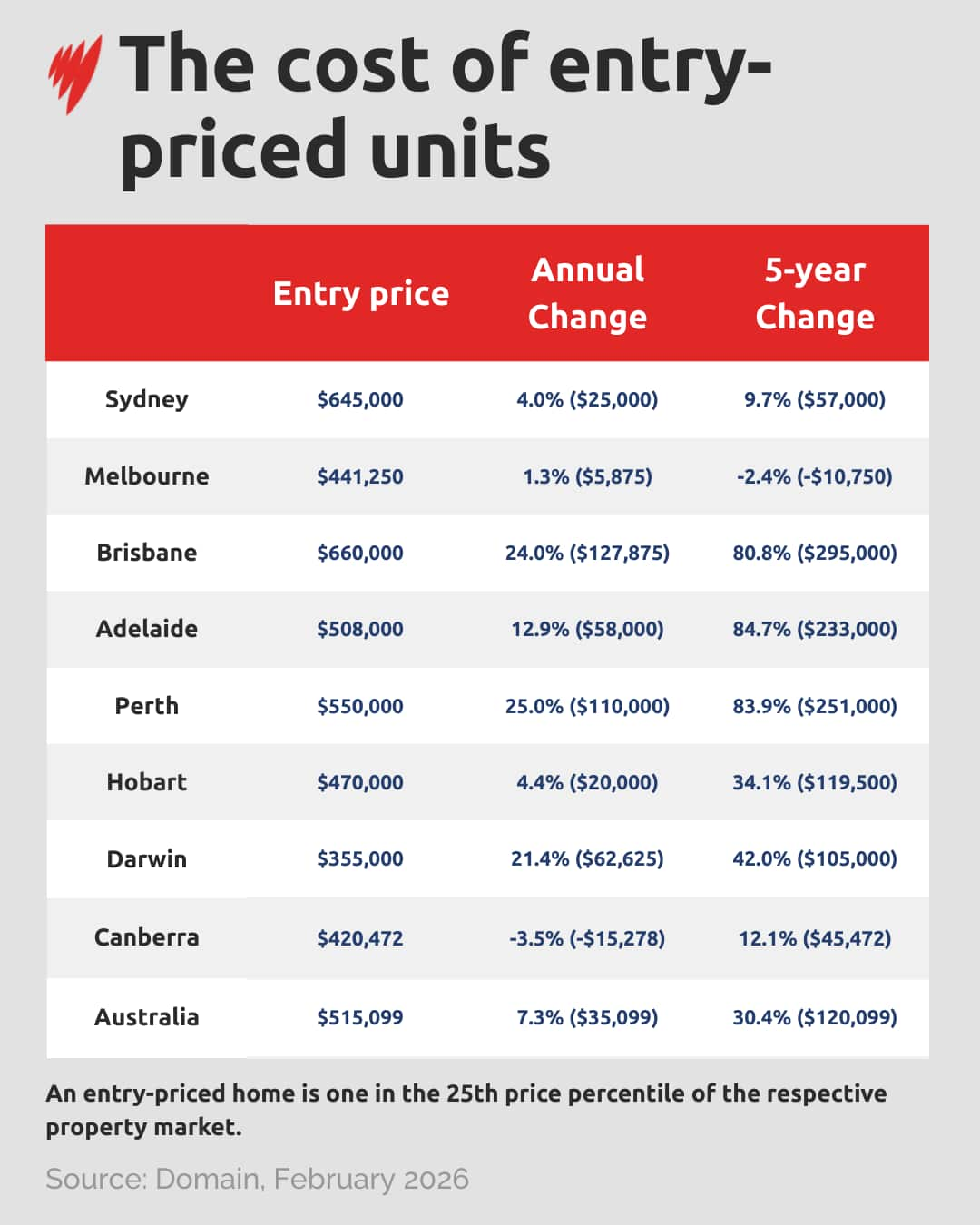

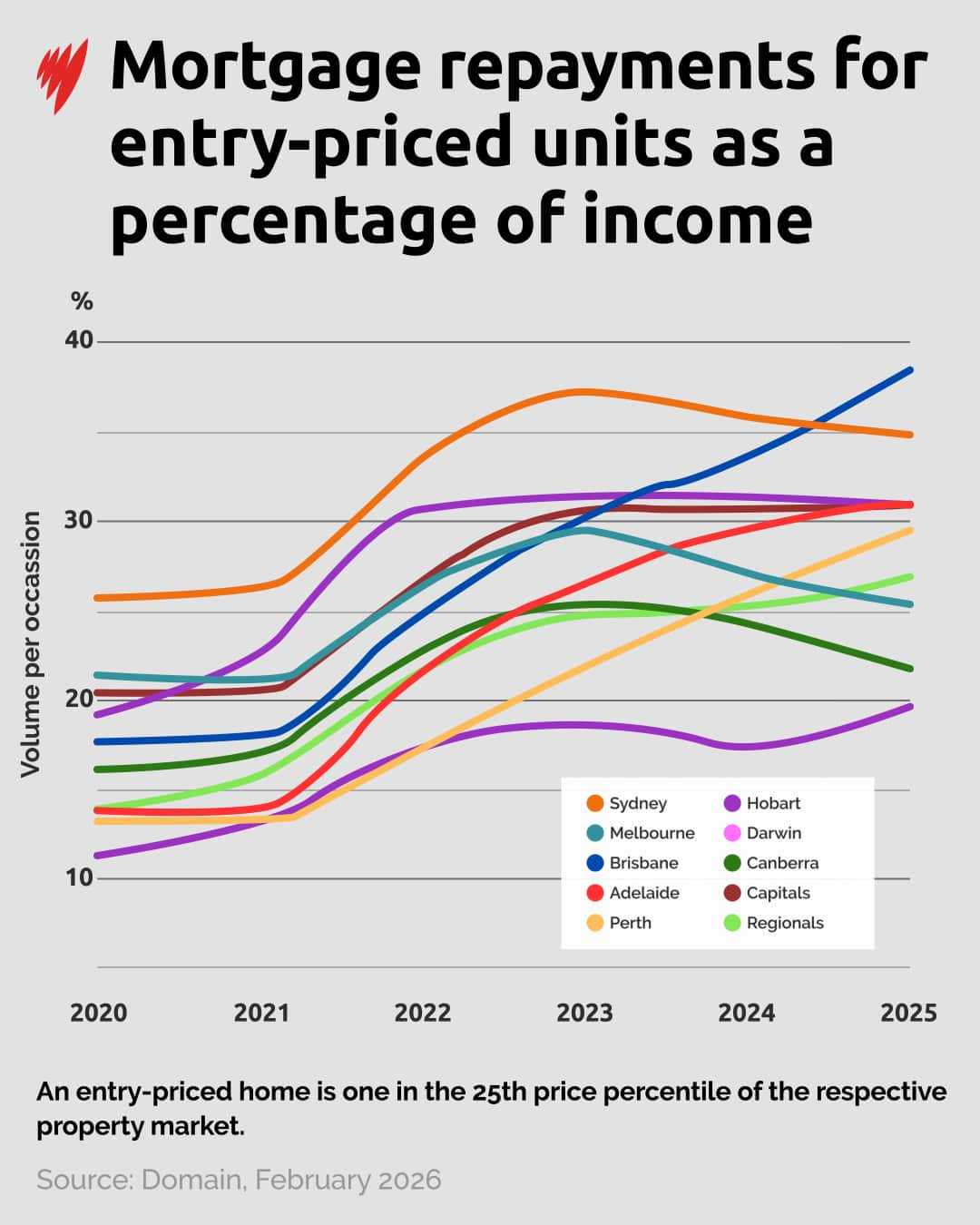

Meanwhile, an entry-priced unit in Australia is up 30 per cent over the same period, up to $515,000.

Sydney is the most expensive city in the country for an entry-priced home at $1,150,000, an increase of $450,000 compared to five years ago.

Adelaide experienced the largest rise in entry-priced houses at $720,000, up 159 per cent or $442,250 over five years.

This spike in price was followed by Brisbane at $856,000, which saw an increase of 106 per cent or $441,000 in five years, while Perth had a narrowly smaller increase with prices resting at $780,000.

Unit costs also increased over the half-decade, with Brisbane overtaking Sydney in entry-level prices.

Queensland's capital recorded a growth of 80 per cent over five years, with entry-priced units increasing by $295,000, ending up at $660,000.

Sydney units are marginally cheaper at $645,000, followed by Perth at $550,000.

Darwin is the cheapest market for both entry-priced houses and units at $565,000 and $355,000, respectively.

Powell said she anticipated prices would continue to rise, but at a "more modest pace".

"Ultimately, we continue to see property prices rise because we have a gross undersupply of housing in every corner of Australia.

"Not only is it now the hurdle of saving for a deposit, but it is also actually the survival of servicing that mortgage once you do have a foot on the property ladder."

Mortgage stress on the rise

Domain's data shows that Australians are spending a higher percentage of their income paying off their mortgage.

The group defines a household as facing mortgage stress if it spends more than 30 per cent of its income on repayments.

"It's quite extraordinary really, when you look at five years ago, where we saw pretty much no city in mortgage stress," Powell said.

"Today, what we've got is all of our capital cities are in mortgage stress for entry houses.

"And when we're looking at units, we've got Sydney, Brisbane, and Adelaide that are technically now in mortgage stress."

While she is aware that interest rate rises could create additional financial pressures, Nicula isn't worried.

"Whether the interest rates rise or drop it's just something that you incorporate in your budget, and it doesn't make such a big difference in my opinion, because the whole house and land is our investment and it's just growing."

For the latest from SBS News, download our app and subscribe to our newsletter.