It's just been named as the best city in the world by Time Out — and a new report has suggested it might also have one of the few suburbs in Australia where it's cheaper to buy a unit than to rent.

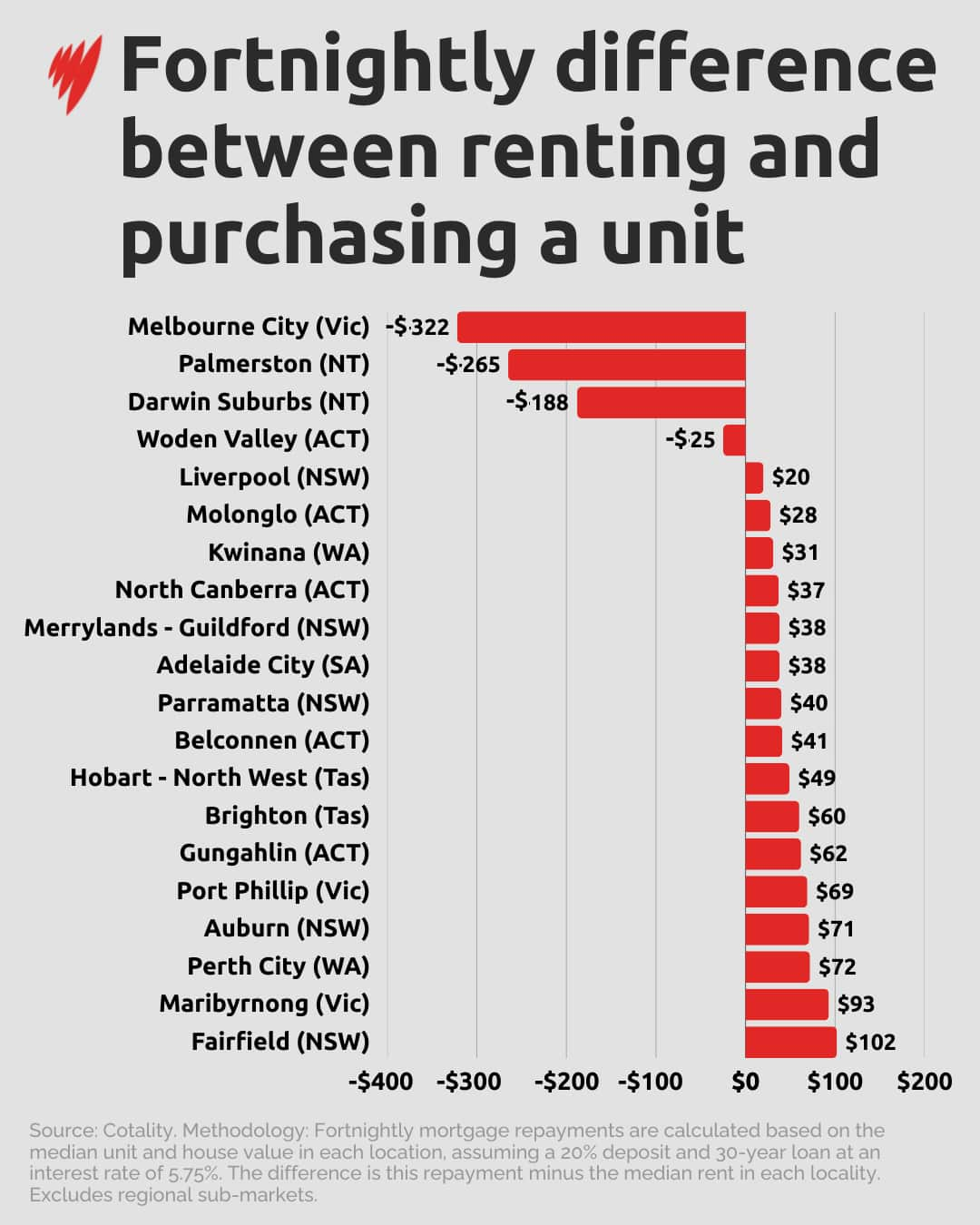

According to Cotality's March housing report, it's $322 a fortnight cheaper to buy a unit in inner-city Melbourne than it is to rent one.

The analysis compared mortgage repayments on median property prices with median rents, with Melbourne City topping the list among capital city regions where buying beats renting.

But before rushing to buy — if you're even in a position to secure a mortgage — experts warn there are a few important caveats that could affect how much you actually pay.

Why Melbourne is such an outlier

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

Melbourne's CBD appears to be one of the few capital city areas where it's currently cheaper to service a mortgage than pay rent for a unit.

Cotality's head of research, Gerard Burg, says the key factor is supply.

"This largely reflects the impact of the rapid expansion in the supply of apartments in the area over recent years," Burg told SBS News.

He said the increase in supply has kept median unit values lower.

Combined with last year's interest rate cuts (one of which has since been reversed), this has lowered mortgage repayments.

"In contrast, rental vacancies in Melbourne have remained quite tight, and that's allowed some upward pressure to rents, which has pushed them above the fortnightly mortgage repayment."

Domain's Nicola Powell said the trend is particularly visible in Melbourne's CBD, Carlton, South Melbourne and Richmond.

"Melbourne has been better than other major capitals in providing apartment and unit supply," she told SBS News.

"The market has been more subdued overall, particularly when compared to other capital cities."

"In the unit sector, we also know that investors were really shying away from Melbourne overall in recent years … All those factors together have helped to contribute to making it cheaper to purchase in some of those inner-city suburbs of Melbourne for units rather than rent."

While Burg warned the trend may be temporary, he said the gap between renting and buying in Melbourne's inner areas was likely to remain.

"We think it's unlikely to persist in the long term. Three out of the four big banks are now forecasting two rate hikes by the RBA … this will directly increase mortgage repayments."

"This may not immediately erode the gap in inner Melbourne, but will likely reduce it."

Where else is it cheaper to buy than rent?

While most locations in Australia still show renting as the cheaper option, there are a few exceptions.

Cotality highlighted two places in the Northern Territory where it's cheaper to service a mortgage than rent a unit.

In Palmerston, it's $265 cheaper, while in Darwin's suburbs, it's $188.

In only one other location, the ACT's Woden Valley, the same situation applies — although it's only a saving of $25 per fortnight.

In Sydney's Liverpool, renting a unit costs just $20 more per fortnight than buying. Parramatta is $40 more, and Auburn $71 more.

North Canberra came in at $37, Adelaide City $38 and Perth City $72.

Those figures assume a 20 per cent deposit on a 30-year loan at an interest rate of 5.75 per cent.

"Parts of Darwin are showing a similar dynamic, but for more comparable east coast cities, we also see it being cheaper to buy a unit in the Woden Valley in the ACT, while it is only marginally more expensive to purchase a unit in Parramatta in Sydney, along with surrounding suburbs," Burg said.

"In the case of these east coast markets, the supply story is quite similar, with large-scale apartment developments keeping the median value of units in these areas contained."

Houses? Not so much...

For houses, however, the picture is different.

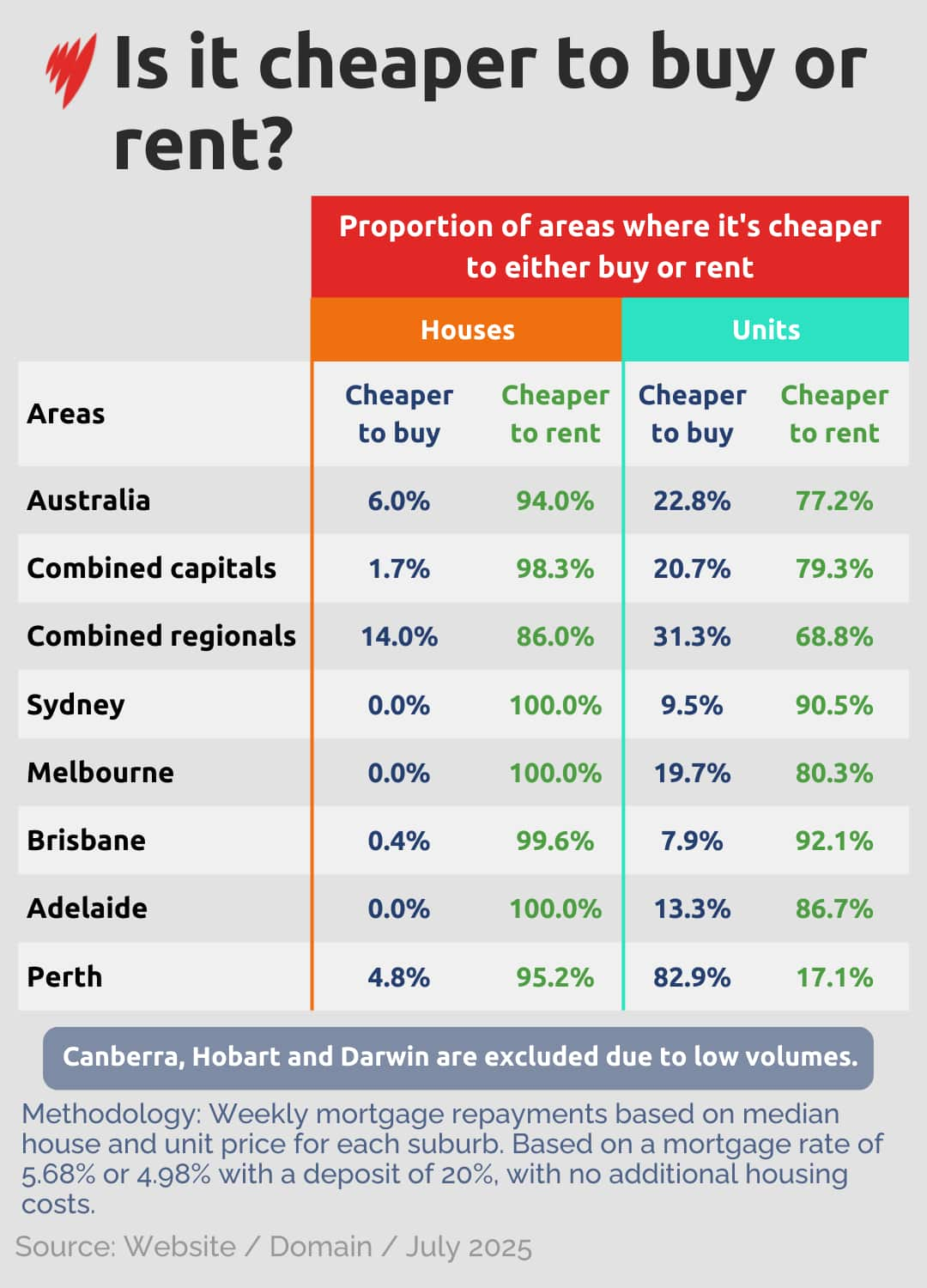

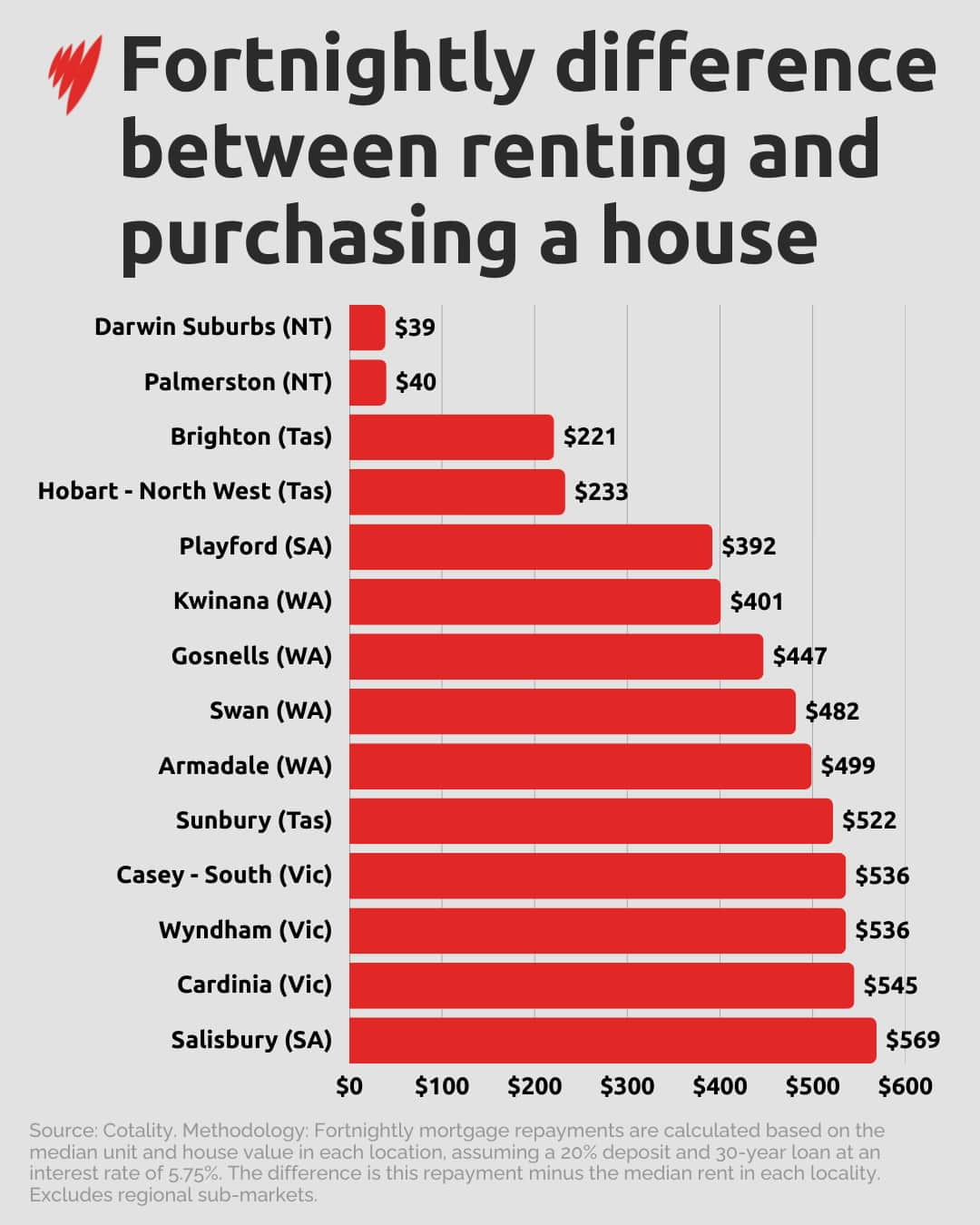

No capital city areas were cheaper to buy than rent, though the smallest differences appeared in Darwin, Hobart and the fringes of Adelaide and Perth.

Outside of capital cities, regional areas offer more opportunities, particularly in mining regions and remote areas.

Research from Domain in July last year found that servicing a mortgage on a house is cheaper than paying rent in just 6 per cent of suburbs.

Across combined capital cities, only 1.7 per cent of suburbs showed it was cheaper to buy a house than rent, compared with 20.7 per cent of suburbs for units.

In regional areas, the numbers rose to 14 per cent for houses and 31.3 per cent for units.

Powell noted these numbers are likely even lower now, given recent price growth and rising interest rates.

So, is rent money wasted money?

Not quite.

The numbers only apply if you're able to scrape together enough money to fork out a 20 per cent house deposit.

A 20 per cent deposit on a $450,000 is $90,000. By contrast, a 5 per cent deposit would be $22,500 — but you'd also be up for additional fees (and higher repayments).

"Being able to switch from renting to buying with a mortgage under this analysis would require the new buyer to have a 20 per cent deposit and finance approval," Berg said.

It also doesn't include other costs of home ownership, including insurance, maintenance, body corporate fees or stamp duty.

"The growth of unit supply in some inner-city markets, or key growth centres (such as Parramatta), does provide some opportunity for renters seeking greater security from ownership, but it certainly isn't as simple as 'rent money is dead money'."

Powell added that smaller deposits will increase the loan size and mortgage repayments, adding that first-home buyers may also need to factor in lenders mortgage insurance and other costs.

"It's really important to do the math," she said.

"Part of that is working out what fits your financial position. Also layer into that what first-home buyer schemes you're potentially eligible for — that helps map your whole journey."

But if you've got the funds, there are opportunities, Burg said.

"At a time when there are heightened concerns around affordability, these pockets may provide an opportunity for buyers who are ready to go."

For the latest from SBS News, download our app and subscribe to our newsletter.