This audio is voiced by AI and may occasionally mispronounce words.

Share your feedback and help us improve this feature. Read more about how we use AI at SBS here.

Melbourne is one of Australia's two global cities — consistently ranked among the world's most liveable — and historically one of the country's strongest property markets. But it is now trailing other capitals. Could that be about to change?

The answer is far from straightforward.

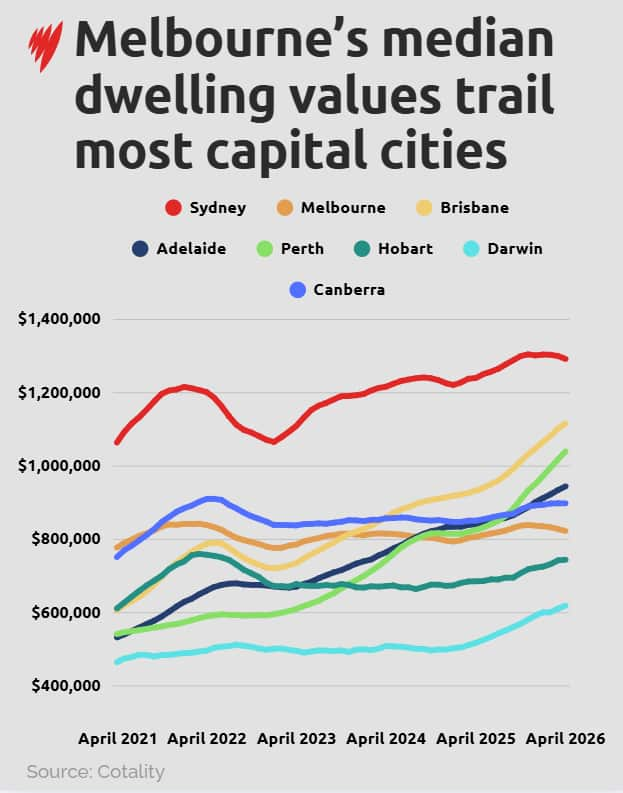

Over the past five years, Melbourne has seen by far the smallest increase in home values of any capital city.

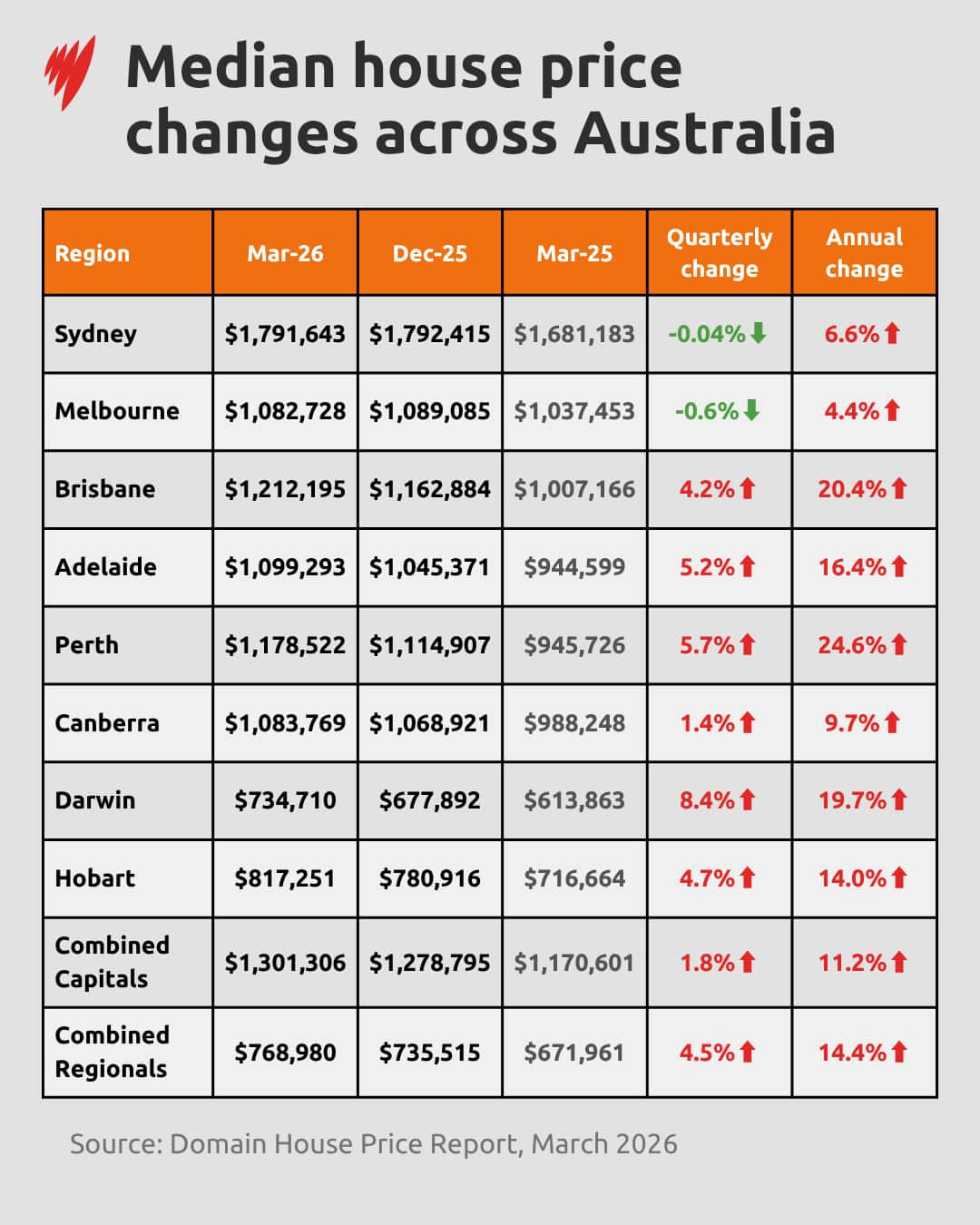

Median house prices in Brisbane, Perth, Canberra and for the first time, Adelaide, have overtaken Melbourne, according to Domain's March quarterly house price report.

Nicola Powell, Domain's chief of research and economics, says the recent declines, while modest, may signal a shift in momentum for Melbourne's market, particularly given its sensitivity to interest rate movements.

News that makes sense

Your trusted source for staying up-to-date with the world around you. Get free daily news updates and analysis, straight to your inbox.

That change highlights how Melbourne's position is evolving: a city long defined by high prices is now, relatively speaking, playing catch-up.

For some property experts, Melbourne's relative affordability presents a possible window of opportunity for buyers.

At the same time, the city's fundamentals are shifting again. Migration to the state has picked up, while construction headwinds suggest housing supply could tighten — a dynamic that analysts say could drive prices upward, creating growth opportunities for investors and further challenging affordability for first-home buyers.

But with possible federal taxation changes in the upcoming budget, economic uncertainty and the prospect of further rate hikes looming, housing prices in Melbourne have again slipped, dropping by 1.5 per cent in the three months to April, according to data from property research firm Cotality.

That short-term decline underscores the uncertainty facing the market: conditions are improving in some areas, but broader economic pressures are still weighing down prices.

ANZ's latest housing forecasts had predicted prices in Melbourne would dip by 1.7 per cent in 2026, compared with a 0.7 per cent fall in Sydney, while Perth (12.3 per cent), Brisbane (9.7 per cent) and Adelaide (5.7 per cent) are expected to post gains.

In other words, even as conditions begin to shift, Melbourne is still expected to underperform its interstate peers in the near term.

So how can Australians interpret these diverging signals?

Why Melbourne has fallen behind

Melbourne property prices fell in 2022 as a rapid series of interest rate hikes slashed borrowing power and cooled demand.

But the downturn was not driven solely by interest rates. The slowdown was likely amplified by changes to land tax that reduced investor appetite, a COVID-19 pandemic-era population decline and, compared to other states, a steadier pipeline of new housing supply.

Together, these factors created a rare convergence: weaker demand alongside a relatively resilient supply.

It wasn't until late last year that median prices in Melbourne returned to — and briefly exceeded — their 2022 peak.

That delayed recovery has widened the gap between Melbourne and faster-growing markets such as Perth and Brisbane, where tight supply and strong population inflows pushed prices sharply higher.

Gerard Burg, Cotality Australia's head of research, says: "We saw a period of outflow of population out of Melbourne and out of Victoria, responding to the lockdowns that we had in place in Melbourne during the pandemic."

"That has now reversed," he tells SBS News.

The return of population growth is a critical shift, but on its own, it's not enough to drive a rapid price rebound. Burg says this is partly because Melbourne's housing supply has kept pace with demand more closely than in other capitals.

"Melbourne is a much better balanced market in terms of supply and demand than particularly Perth and Brisbane, and to a lesser extent, Adelaide as well."

'It's a story about affordability'

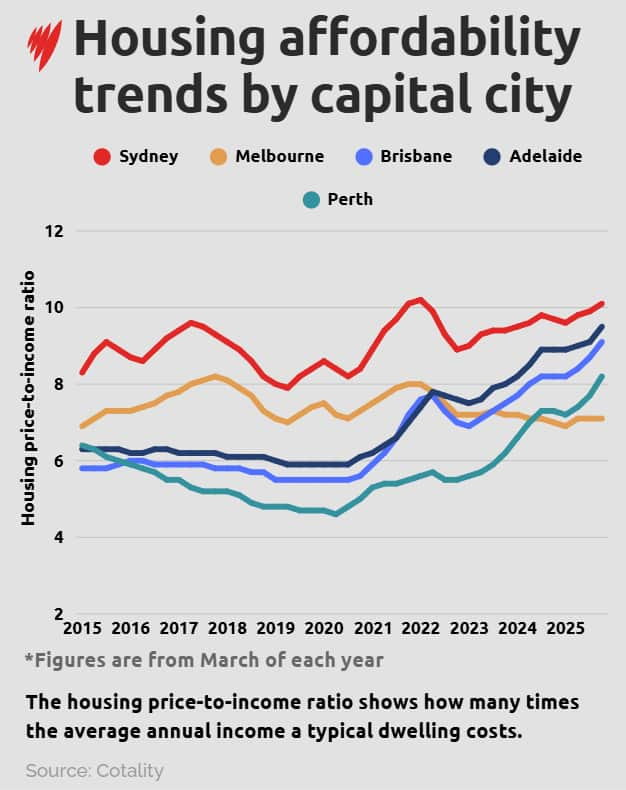

Melbourne and Sydney were once Australia's least affordable cities, particularly when measured against household incomes, a key benchmark for housing stress.

Since 2022, Perth, Brisbane and Adelaide have all overtaken Melbourne as their price-to-income ratios surged.

That reversal has quietly repositioned Melbourne in the national housing conversation from one of the most stretched markets to one that now offers a relative affordability buffer.

In Sydney, a typical dwelling cost just over ten times the average annual income in March last year, according to Cotality data. Adelaide ranked second at 9.5 times, followed by Brisbane (9.1), Perth (8.2), Hobart (7.6) and Melbourne (7.1).

The gap is significant and it's starting to influence where Australians choose to live.

"The last three quarters, we have seen net [population] inflows into Victoria," Burg says. "And I think that really is, as much as anything, it's a story about affordability.

"So the fact that Melbourne home values are comparatively affordable … some people seem to be voting with their feet in that regard."

That shift aligns with what many housing economists have been pointing out, that relative affordability, rather than outright prices, is now driving migration and demand across the country.

Conflicting signals cloud the market

Burg says the Melbourne market presents "mixed signals".

On one hand, there are early signs of softness. Demand has eased, he says, and could weaken further given rising interest rates and ongoing uncertainty around energy prices and inflation. Listings have also crept higher, with the supply of existing properties for sale above the five-year average.

On the other hand, interstate migration trends are moving upwards, in part because Melbourne presents a "sizeable affordability advantage" over most other capitals.

At the same time, rising construction costs are affecting the feasibility of new construction — from a profitability perspective — which could constrain supply and drive house prices upwards.

"Given where median values are right now, you build a new house on a block of land — are you going to return a profit? Basically, it's a lot easier to do that construction right now in a market like Brisbane or Perth, for example, where the values have risen so rapidly," Burg says.

Analysts warn that, if construction slows as population growth returns, the market could tighten sooner than expected.

Given those factors, "you can see a scenario there where Melbourne could be an outperformer over that sort of medium-term period", Burg says.

Importantly, Melbourne's softer price growth is not solely a sign of weakness. While it has often been presented as a negative story, Burg says "a large part of it reflects Victoria leading the country in terms of dwelling completions over this period, with a sizeable share being stand-alone houses".

"So this modest increase in values over this period is a negative from an investor point of view, but it is a positive from a first home buyer perspective," Burg says.

"The dollars of a first home buyer in Melbourne go a lot further than in almost any other city."

'Green shoots' emerge but market likely to be 'choppy'

While the market has shown signs of "green shoots", it's likely it will remain "choppy" for the foreseeable future, amid economic headwinds and forthcoming changes to capital gains tax and negative gearing in the May budget, according to Lachlan Delahunty, founder of property investment advisory firm Follio and host of the Follio Property Podcast.

"But I look at Melbourne now as a medium-to-long term play," he tells SBS News.

He said that, considering what he predicts over the next three to 10 years, Melbourne's current value opportunity is striking.

I think this is a moment in time we'll look back in hindsight and say, 'Wow, I can't believe Melbourne got that affordable'.

He says Melbourne's fundamentals are strong.

"You've got very strong population growth. You've got days on market declining significantly … showing me the demand's improving," he says.

Median rents have also trended upwards, making the market more attractive to investors.

'Challenging dynamics' ahead for first home buyers

Victoria has been one of the leading states for first home buyer activity across Australia, "and that is because it's had generally more subdued housing market conditions", says Powell from Domain.

"When it comes to property decisions, a better decision is made when you take your time, irrespective of what type of buyer you are," she tells SBS News.

"Decisions made under rush conditions when you've got a market that is peppered by FOMO (fear of missing out) don't necessarily mean that you make the best decision for your circumstance.

"So I do think when the market starts to slow down, it can provide greater clarity for buyers and give them time to make their purchasing decisions."

However, she warns there may be "challenging dynamics" ahead, with softer market conditions and the prospect of further interest rate rises potentially creating risks for recent first home buyers, particularly those with limited financial buffers.

"You obviously then don't want to get in the position where you've got negative equity," she says, referring to a situation in which the unpaid balance on a mortgage exceeds the market value of the property which the loan was taken out to purchase.

What that paints for a first-term buyer is to make sure they build in a financial buffer to ride the potential of two more rate hikes coming through.

Taken together, Melbourne's housing market is still pulling in different directions.

Short-term pressure persists, but improving population growth and relative affordability suggest conditions could stabilise and gradually strengthen over the medium term.

For the latest from SBS News, download our app and subscribe to our newsletter.